Most of them are ranged between 4 to 6% pa. Hyflux is issuing theirs at 6% and subsequently stepped up to 8% pa if they did not redeem by April 2018. But the company issuing these preference shares are banks, which are ranked above normal companies in my opinion, so naturally Hyflux will have to offer a higher yield to account for their more risky circumstances. Banks are financial institutions that are integral to a country and they must not be allowed to fail, especially in Singapore's case, lest the public's confidence in the financial system be wavered. Can the same be said for Hyflux? No matter how good the terms of the preference shares are, if the underlying company that issued it sinks, all the high yield offered are moot. I can't tell what I'm going to eat for lunch later, so I don't have the predictive powers to determine if Hyflux is still going to be around in a few years time to give me my dividend.

I would have thought that people who preferred preference shares are those who do not want to worry so much about the ups and downs of the market, since if they had bought it at par value, the shares would also be redeemed back at par value too, so the fluctuations of the price in between does not matter to them. In the meantime, they just have to collect the dividends and live their own life. Would they care to look closely at how the underlying company is doing from time to time? I would think not, because such investors should want a fuss free kind of passive income. Would hyflux offer such a safe, fuss-free haven, being the underlying company issuing the preference shares? I do not know, but I would bet my money on the banks anytime if I truly want a fuss-free kind of investment instrument. Besides, I do have a preference share by HSBC bought below par value, at a rate of 6.4% pa (but denominated in USD). I do not even care about what the price of the shares, which is exactly what I like about preference shares. If any preference shares that I bought do not give me this kind of feeling, I would avoid.

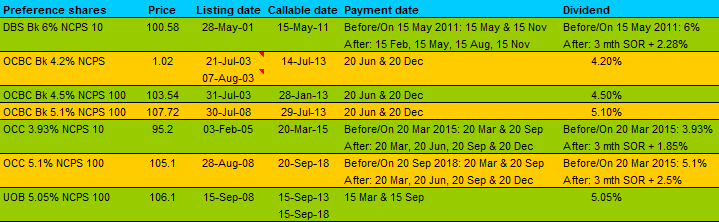

The dividend yield for Hyflux is around 2.5-3% pa. Do you wonder why it is low? Hyflux is a growth company, hence the need for cash necessarily reduces the amount given as dividend. They must obviously think that they can give you a better returns for the cash than you could. The good thing about putting your money into the ordinary shares of Hyflux is that you can participate in the upside of the company's growth. If the earnings of the company grew, the price will also rise (eventually). The bad thing is that if all these scenario didn't come to fruition, you'll end up with a possible loss. On the other hand, buying the preference shares limit the upside in terms of price appreciation. Preference shares do not move too much upwards, though it can certainly plunge downwards. Just take a look at the preference shares of the various banks during the financial crisis. The downside for preference shares is limited though, unless the underlying company fails catastrophically, because the lower the share price, the higher the yield will be. There will come a point in time where the yield is so attractive that buyers will step in to stop the downslide. If you buy at par value and hold it until redemption, there will be no capital loss at all.

My point 4 in this post on preference shares still sums up my decision on this one. I would look at it only when the price goes below the par value. I think you can still make money out of this (in fact, I think it might be a good stag). Given that you can even use up to 35% of your investible savings in CPF (the balance in CPF ordinary account plus the net amount withdrawn for education and investment) to apply for this and get a yield higher than what the CPF rates can give you, it might be worthwhile to invest some money into it.

So there, the odds are laid out in front of you. Go ahead and decide what to do with your money.

*This article is contributed to IM$avvy financial portal, which is managed by Central Provident Fund Board and supported by MoneySense. This site has a noble aim of promoting financial literacy to the general population.

3 comments :

Hi LP,

Well argued. However, if price falls below par and gives a higher yield, I might be too afraid to get some then. Why would the price fall below par, I would wonder?

Now, if DBS preference shares should go below par, I would close both eyes and buy. ;p

Hi AK,

Haha, I agree..must depend on the circumstances leading to the selldown :) Just the other day, sfry mentioned that the SIA bond is selling below par :)

Thanks for dropping by :)

Well, AK71, the banks' prference shares DID fall below par before, but did you dare to buy any then? :)

Post a Comment