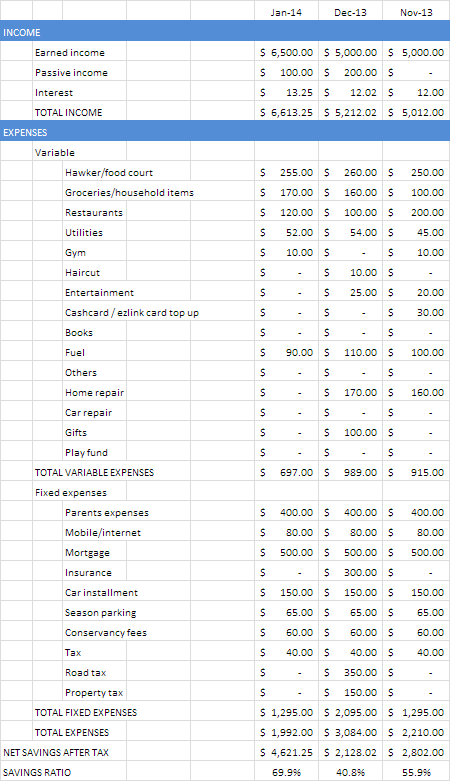

The next report to look at is the balance sheet. This shows how your liabilities are like against your assets, and also the breakdown of the liabilities and assets. The sum of your assets minus your liabilities will be the book value of a company. In terms of your personal balance sheet, this is known as your net worth. I know there are a million ways to calculate net worth, so it's up to you to decide which definition you want to adopt. It doesn't really matter as long as you keep the standards the same when you compare yourself against different time periods. Just don't change the yardstick all the time. It'll be like a company that changes their way of valuating their biological assets or the rate of depreciation or their accounting period.

It's important to know that similar to the balance sheet of a company, a personal balance sheet is a static picture of a company's assets and liabilities at a particular point in time. The balance sheet of a company taken at different times will likely be different. Just pick a time period that is significant. I think doing a balance sheet monthly is kind of pointless, because there isn't much changes in the items (though I still do it). A comparison of your personal balance sheet across different years should be good enough.

Anyway, this is the way how I calculate my net worth:

Net worth = All bank accounts + cash + money market funds + surrender cash value of whole life + marked to market value of stocks + scrap value of car + CPF - (car loans + credit card debts)

Notice that I did not include the marked to market valuation of my residential property , but neither did I include the loans that I borrowed to buy that property. The mortgage payment part is included in the income statement and I'm contented to treat it this way. As mentioned, there are a lot of ways to do your net worth, so just pick something that works and make sense to you.

A company that can withstand financial stresses are those that are light on debts. But more importantly, it's whether the company can service their debts without breaking a sweat. You can thus calculate a variety of ratios, each of which can be used to analyse how robust you are to financial stress. Here's but a few:

1. Years to service debt

I don't care how others define the ratio, but this is what make sense to me. My way of calculating is this: (All loans and debts - cash/cash equivalent - 50% market to market value of stocks) / (net savings per year). I do not include CPF because I don't use that to pay off my housing loans. For someone who does, you can easily tweak the formula to include all the cash that you can use to pay off the housing loans from your CPF accounts. Basically, the aim is to only use those money that are liquid enough to subtract off your total debts in the numerator of the formula. There's no point deluding yourself that you have a lot of money stuck in some illiquid asset, say like your cpf account, but those can't be used to pay off your debts when crunch time hits. I also did not include the full marked to market value of the stocks to account for the fact that when the shit hits the fan, your portfolio value will also drop. You can still liquidate it but it won't be at the price you want to sell.

For example, in the balance sheet above for 2013, the housing loan is about 430k and car loan is 7.2k, total being 437.2k (let's ignore credit card debts, which isn't significant). Subtract off all my cash/cash equivalent plus 50% of portfolio value gives me 353.7k . If my savings per year is 30k, 353.7/30 = 11.8 years. This means that if I dedicate all my liquid assets to the repayment of debts, I should be debt free in 11.8 years. Probably shorter than that, since I didn't include my wife's contribution in the savings. I think what's more important is that while the debts and liabilities are certain, my income and hence the savings are not certain. Can I save that much for another 11.8 years? If not, then I better accelerate it, work harder and save harder to bring the ratio down. It's also silly to sell of everything and use all the cash to pay off the debts. This is just a stress test scenario to see if you can withstand financial difficulties.

If you have a negative number, congrats! That means that your debts can probably be covered by your liquid assets. You have a healthy balance sheet!

2. Current ratio

Current ratio is current assets over current liabilities. This will see whether you have problems paying off things like credit cards, income tax, annual insurance premium and very near term loans. I'll treat current assets as cash/cash equivalent (like money in money market fund, fixed deposit, savings account etc). If you have this ratio being less than 1, better watch out. Again, relative numbers are more important than absolute numbers. If last year your ratio is 1.1 and this year, it's 0.8, you should go and find out what is happening in your financial health. It doesn't mean that there's something wrong and you should correct it, but it's could be a symptom of something bad that could be coming.

3. Liquid vs illiquid assets

Liquid assets are those assets that can be easily converted to cash. Illiquid ones are those that need a long time to convert to cash. Things like property can be rather illiquid. Stocks are liquid, but they might not be able to sell at the price you want when you need to sell it. The really liquid ones are cash /cash equivalent and money market fund. CPF accounts are not liquid at all, unless you're near the withdrawal age. I'm rather ambivalent about cash surrender value of whole life insurance plan. It's not that it's illiquid, but I'll rather treat it as untouchable.

This ratio will allow you to analyse whether you are one of those cash poor, asset rich folks who have a lot of their net worth locked up in things that do not generate cash. You might have a property worth 1 million dollars but you can't really break off a brick to pay for food. I suppose when we get older, we need to see this ratio gearing towards the liquid side, because we no longer have a income stream from work due to retirement / retrenchment.

It's important not to look at just one slice of your financial health to conclude whether you are well off financially or not. Looking at just the balance sheet does not give you a full picture. For example, consider a scenario where there is a person with high net worth. His personal balance sheet consists of large assets and very little debts. However, his balance sheet has a large percentage of the assets that are fixed (i.e. illiquid) with very small percentage in current assets, like cash or cash equivalent. Though this person may have a strong balance sheet, he might not be able to live comfortably day by day because he has very poor cash flow. If his cash flow is insufficient to pay off his expenses, specifically his debt commitments, he might even have to sell of his fixed asset in order to generate that cash flow. We have to look at the income statement too to see a better picture of his financial health.

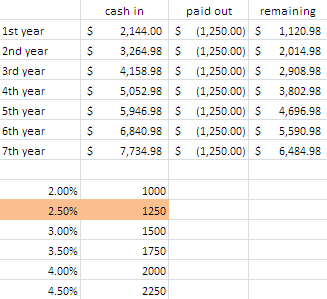

It's important to know that similar to the balance sheet of a company, a personal balance sheet is a static picture of a company's assets and liabilities at a particular point in time. The balance sheet of a company taken at different times will likely be different. Just pick a time period that is significant. I think doing a balance sheet monthly is kind of pointless, because there isn't much changes in the items (though I still do it). A comparison of your personal balance sheet across different years should be good enough.

Anyway, this is the way how I calculate my net worth:

Net worth = All bank accounts + cash + money market funds + surrender cash value of whole life + marked to market value of stocks + scrap value of car + CPF - (car loans + credit card debts)

Notice that I did not include the marked to market valuation of my residential property , but neither did I include the loans that I borrowed to buy that property. The mortgage payment part is included in the income statement and I'm contented to treat it this way. As mentioned, there are a lot of ways to do your net worth, so just pick something that works and make sense to you.

|

| An illustration of how the personal balance sheet is compared across years |

A company that can withstand financial stresses are those that are light on debts. But more importantly, it's whether the company can service their debts without breaking a sweat. You can thus calculate a variety of ratios, each of which can be used to analyse how robust you are to financial stress. Here's but a few:

1. Years to service debt

I don't care how others define the ratio, but this is what make sense to me. My way of calculating is this: (All loans and debts - cash/cash equivalent - 50% market to market value of stocks) / (net savings per year). I do not include CPF because I don't use that to pay off my housing loans. For someone who does, you can easily tweak the formula to include all the cash that you can use to pay off the housing loans from your CPF accounts. Basically, the aim is to only use those money that are liquid enough to subtract off your total debts in the numerator of the formula. There's no point deluding yourself that you have a lot of money stuck in some illiquid asset, say like your cpf account, but those can't be used to pay off your debts when crunch time hits. I also did not include the full marked to market value of the stocks to account for the fact that when the shit hits the fan, your portfolio value will also drop. You can still liquidate it but it won't be at the price you want to sell.

For example, in the balance sheet above for 2013, the housing loan is about 430k and car loan is 7.2k, total being 437.2k (let's ignore credit card debts, which isn't significant). Subtract off all my cash/cash equivalent plus 50% of portfolio value gives me 353.7k . If my savings per year is 30k, 353.7/30 = 11.8 years. This means that if I dedicate all my liquid assets to the repayment of debts, I should be debt free in 11.8 years. Probably shorter than that, since I didn't include my wife's contribution in the savings. I think what's more important is that while the debts and liabilities are certain, my income and hence the savings are not certain. Can I save that much for another 11.8 years? If not, then I better accelerate it, work harder and save harder to bring the ratio down. It's also silly to sell of everything and use all the cash to pay off the debts. This is just a stress test scenario to see if you can withstand financial difficulties.

If you have a negative number, congrats! That means that your debts can probably be covered by your liquid assets. You have a healthy balance sheet!

2. Current ratio

Current ratio is current assets over current liabilities. This will see whether you have problems paying off things like credit cards, income tax, annual insurance premium and very near term loans. I'll treat current assets as cash/cash equivalent (like money in money market fund, fixed deposit, savings account etc). If you have this ratio being less than 1, better watch out. Again, relative numbers are more important than absolute numbers. If last year your ratio is 1.1 and this year, it's 0.8, you should go and find out what is happening in your financial health. It doesn't mean that there's something wrong and you should correct it, but it's could be a symptom of something bad that could be coming.

3. Liquid vs illiquid assets

Liquid assets are those assets that can be easily converted to cash. Illiquid ones are those that need a long time to convert to cash. Things like property can be rather illiquid. Stocks are liquid, but they might not be able to sell at the price you want when you need to sell it. The really liquid ones are cash /cash equivalent and money market fund. CPF accounts are not liquid at all, unless you're near the withdrawal age. I'm rather ambivalent about cash surrender value of whole life insurance plan. It's not that it's illiquid, but I'll rather treat it as untouchable.

This ratio will allow you to analyse whether you are one of those cash poor, asset rich folks who have a lot of their net worth locked up in things that do not generate cash. You might have a property worth 1 million dollars but you can't really break off a brick to pay for food. I suppose when we get older, we need to see this ratio gearing towards the liquid side, because we no longer have a income stream from work due to retirement / retrenchment.

It's important not to look at just one slice of your financial health to conclude whether you are well off financially or not. Looking at just the balance sheet does not give you a full picture. For example, consider a scenario where there is a person with high net worth. His personal balance sheet consists of large assets and very little debts. However, his balance sheet has a large percentage of the assets that are fixed (i.e. illiquid) with very small percentage in current assets, like cash or cash equivalent. Though this person may have a strong balance sheet, he might not be able to live comfortably day by day because he has very poor cash flow. If his cash flow is insufficient to pay off his expenses, specifically his debt commitments, he might even have to sell of his fixed asset in order to generate that cash flow. We have to look at the income statement too to see a better picture of his financial health.

.jpg)