Recently a person named newbie shared some of his insights into leveraging for passive income. It's not a new concept to me, but he did kindly shared some of the details on how he did it. Many thanks and appreciation for his generous sharing in my infamous cbox. Before I proceed, do take note that I've never done it before and this is at best an interpretation of what I had gathered from his sharing. It may not be exactly what he had in mind because some of the information might be lost in translation, but I believe the gist of it is captured here. Any mistakes posted is solely my own and please do read the disclaimer at the bottom of the site if you decide to act on this information.

The idea can be summarized in a line:

Borrowing at a cheap interest rate and using the money to buy a stable financial instrument that is paying a higher interest rate, thereby earning the difference between the two.

As in all decisions regarding financial investment, the devil lies in the details. Several questions comes to mind. I don't profess to have the answers to all but this is what I've gathered from our conversations.

1. How cheap is the borrowing? Where to get such cheap money?

He mentioned that cheap financing is available from margin facilities in certain brokerage. From my understanding, if you're a private banking client, you can have access to cheap financing too. These will lend you different currencies at different rates, say USD at 2% pa or SGD at 1.5% pa (the figures are for illustration purpose only). Of course, not everyone is a private banking client (you need to satisfy a minimum asset requirement), but you and me can get cheap financing too. Newbie offered a suggestion of the possibility of getting a lower than 2% pa balance transfer for 6 months, thereafter it's a matter of rotating between different banks after every 6 months to enjoy the preferential borrowing rates.

The thing is, after you had reached a certain amount of assets, you start to have more options available to you that is not available before.

2. What is stable financial instrument? How much higher interest rate can you get from it?

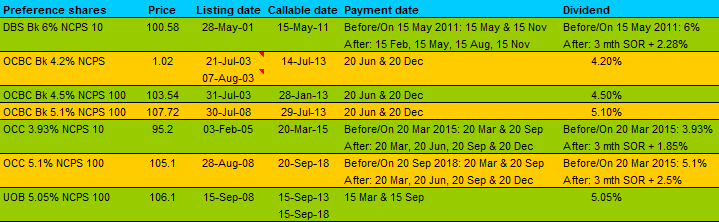

Stability here means that the price do not move much. It is risk defined in the academic sense, and the lower the price volatility, the more stable the instrument is said to be. At the same time, there is a second criteria to fulfill. The instrument must also have high yield. What fits into this then? There are broadly three asset classes - stocks, bonds and preferred shares. Not all stocks satisfy this criteria of stability. But some examples like singpost and perhaps SPH might fit this well. Bonds are preferable because of the call back function upon maturity, so the price movement in between listing and the callable date is immaterial, which thus places the focus solely on the yield. Preferred share (or perps) is an equally good option because of the possibility of getting back the capital upon maturity, and thus removing totally the price volatility factor from the equation to consider.

I think high yielding perps by banks (ranging from 6-8%) are good for such purposes. Newbie did mention something important too - he do not wish to dabble in forex risk, hence the currency he borrowed and the financial instrument must be in the same currency denomination. For example, if you borrow SGD at 1.5% pa, you will buy a bond denominated in SGD at say 6% pa, and not another instrument denominated in USD at 6% pa. This eliminates forex risk and reduces the number of factors to consider.

3. What about the payment of interest and the principal borrowed?

For this type of leveraging, the securities that is bought with the borrowed money is pledged as the collateral, hence there is no need for downpayment or even monthly payment of interest/principal, IF you so wish. I think you'll have to work out the sums yourself if you choose to roll over the interest payments and see if it's worthwhile to even begin doing such things. Of course, you can always make principal payments month to month, using the net interest generated, and eventually get the collateral pledged as free. That is not unlike the pillow strategy used by bro8888 but with a twist - that is the use of leverage.

There is also the very real risk of a margin call, which happens when the value of the collateral goes below a certain percentage of the borrowed amount. If that happens, there will be a margin call to top up cash to lower down the ratio to the acceptable level. The way to mitigate this is to cut loss at a determined level, or simply to use the net interest generated to redeem the principal from time to time, hence raising the limit before a margin call comes in. Besides the risk of the value of the collateral dropping, there is also the matter of increment in interest for the money borrowed. However, this is not going to come overnight so there will be time to react. For example, if you borrowed USD at 2% pa to buy a bond at 6% pa, it might take a few years before the interest of the borrowed amount of 2% will reach 6%, thereby reducing the net interest earned.

Newbie reminded me that at the end of each day, each collateral is marked to market price, so there's a real need to be meticulous in the record keeping to ensure that there will not be a margin call at all. Not for the tardy person.

4. What are the risks involved? Too good to be true it seems...

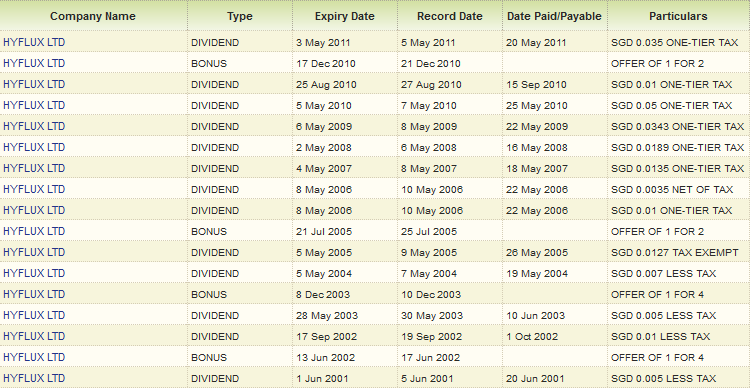

First there is the risk of interest rate increasing. That will cause the interest that you can borrow to increase, hence reducing the net interest that you get. Secondly, there is the risk of the securities dipping in value, thus causing a margin call or a forced sale of the securities in order to maintain the margin ratio. Thirdly, there is the risk of the underlying company of the securities (for example, the underlying company of the much talked about Hyflux preference shares is Hyflux) going belly-up, rendering the securities un-tradable for unspecified period of time.

I think the third risk is the hardest to mitigate, because from history, even the most stable company can cave in. Even if you buy the most stable banking institutions, the one that is 'too big to fail', black swans event can happen most unexpectedly despite the most scrutinizing study of its financial statements.

That being said, will I get involved in this kind of leveraging? I might, but certainly not now. I'll keep my options open and concentrate on getting my main income going up, because my risk for my main income is the lowest, since I know exactly what I'm getting into. I think if you know what you're doing when leveraging, it can be a powerful weapon to advance your financial goals. Just be aware of the risks and mitigate them as well as you can. Thanks again for newbie for this eye-opener way of getting passive income.