This morning, I was quite excited to receive news of another retail bond. This time it's from Hyflux. The last they did that was in 2011 and I made a 4 part series on preference shares

here. Back then, they are issuing 6% cumulative, non-convertible, non-voting and perpetual preference shares. This time, this issue seems more like perpetual shares than bonds. The difference is not significant though, given that it's a perp, so there is no maturity date even though there is a optional but not obligated redeemable date.

Terms of the security

The terms of the perps is spelled out very clearly in the announcement

here:

1. Public offer of up to 230 million (can go up to 250 million), out of total size of 300 million (can go up to 500 million) if oversubscribed

2. Opens on 18th May, close on 25th May noon

3. Min amount is $2k, thereafter in multiples of $1k.

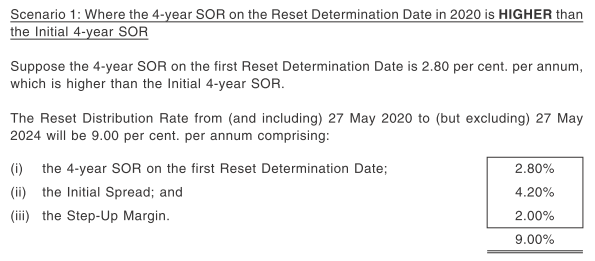

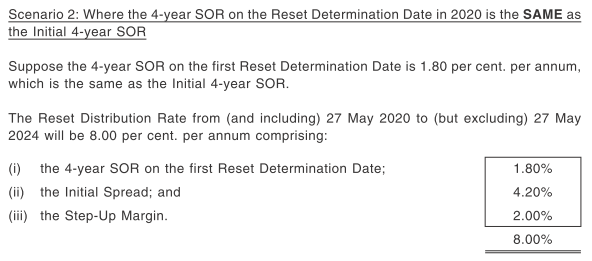

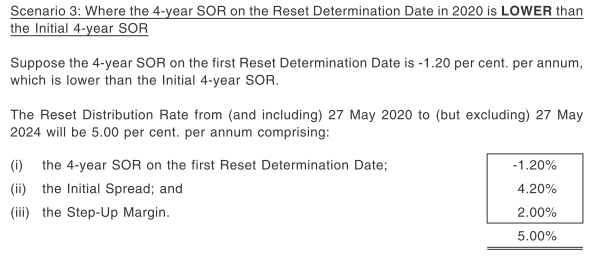

4. This is the interesting feature about the issue. They are giving 6% pa, paid semi-annually (on 27th May and 27th Nov every yr) for first 4 yrs until and excluding 27th May 2020. From 27th May 2020 (inclusive), it'll not be 6% pa anymore, but will be at reset distribution rate.

Reset distribution rate = 4 yr SOR on the reset date + 4.2% pa, + step up margin of 2% pa

They gave excellent illustration for 3 different scenario after 2020 to 2024, shown below:

5. From 2024 onwards, the distribution will be reset again using the formula shown in point 3, but with a new 4 year SOR rate at the reset date in 2024.

6. Is there guarantee of payment if you're a holder of the security? The prospectus states that "each security

confers a right to receive distribution on its outstanding principal amount from the issue date at the applicable distribution rate". The word 'right' doesn't sound right. It offers them a possibility to defer distribution under certain conditions and is no way guaranteed. Reading further from the prospectus, it mentioned that the issuer may elect not to pay a distribution (or to pay a part of) by giving ample notice. They may not elect to defer any distribution if 6 month before the scheduled distribution payment date, one or both of the following occurred:

a. A dividend is paid to its junior obligations. I take junior obligations as the ordinary shares of Hyflux. I may be wrong.

b. If the junior obligation is redeemed, reduced, cancelled or bought back.

This means that if they give out dividends in their junior obligations (I take it as the ordinary shares of Hyflux, which I may be wrong), and/or they did not redeem, cancel or bought back all the junior obligations in a period of 6 months before the distribution payment date, they cannot defer distribution to this security.

Don't ever think they are obligated to pay holders of this security. You have a right to receive but they are not obligated to do so under the stated conditions. But it's not as bad.

They have a feature in this issue that is quite similar to any cumulative pref shares or bond. If they did not pay out any distribution in full or in part, that portion that is not paid out will be placed under arrears of distribution. They will have to pay out the arrears, plus any distribution, by the time they redeem back the securities, or by the next distribution payment date, or before they wind up, whichever comes earlier. If not, they cannot declare or pay dividends to its junior obligations or to redeem, back buy, cancel, reduce it.

I think in simple layman's language, it just means that they must pay out the dividends on the distribution date, unless they are also not giving dividends to hyflux ordinary shares/bond/pref shares holders. That is your sort of guarantee that they will pay out what they should pay out.

7. First redeemable date is on 27th May 2020, which is about 4 years from now, at the par value. They have to redeem all the outstanding amount or none at all. Thereafter, on each distribution payment date, meaning 27th May or 27th Nov after May 2020, they have an option to redeem back too. As mentioned earlier, this is a perp, so there is no fixed maturity date.

Financial strength of Hyflux

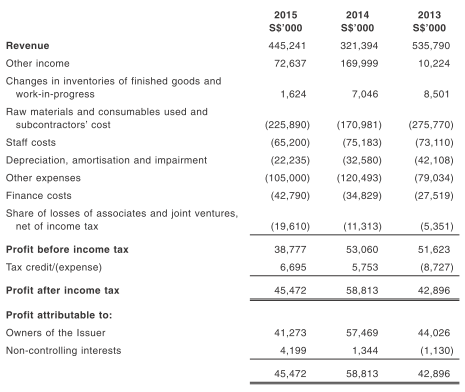

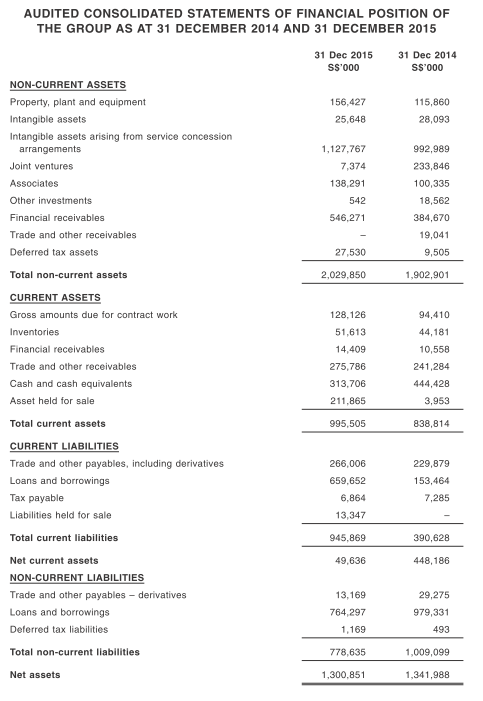

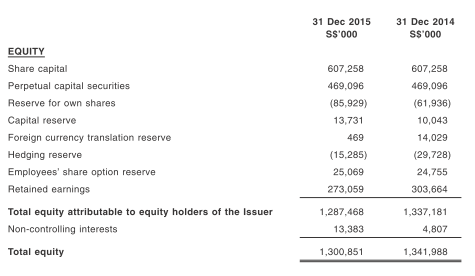

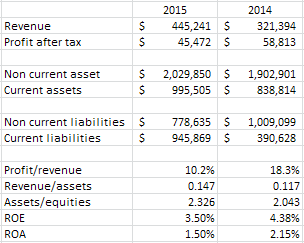

Alright, so far that's just the details of the perp. It's quite a complex issue, if you ask me. My initial excitement becomes a lot more muted once I took a look at Hyflux results.

Debts debts debts. Just mountains of them. I think they are rolling about in their notes and preference shares debts, issuing new ones to redeem older issues. Even this current issue is to redeem back the older issued notes. Specifically, 91.66% of the proceeds is to be used for the repayment of the $100 million 3.5% notes done in July 2008 and updated on Jan 2016, and another $175 million 4.8% outstanding perps (this is not the retail 6% one).

I'm too lazy to dig out past 10 yrs of financial statements, so using the last 2 yrs should suffice:

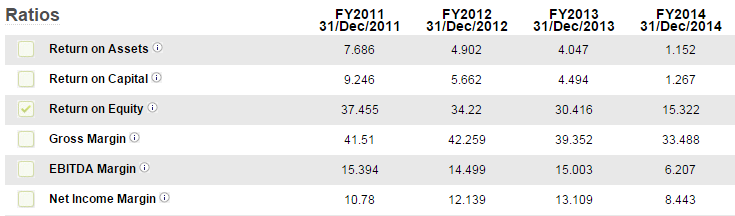

With a ROE of 3.5% in 2015, this isn't a company that I would have invested. But the pref or bonds issued might be a different story. Are they highly leveraged? Below is the ROE for Oxley. They also recently issued a new bond less than a year after their had their first retail one.

Looking at their financial leverage (Assets/equities), Oxley is the more leveraged one, but they are different industry of course. There really isn't a direct comparison for Hyflux. The question is, can they survive for 4 years or more and continue giving dividends to their ordinary shares as well as their bond/perps holders? I'm not confident. Revenue is contract and order based, so a bit lumpy. Even with their leverage, their ROE is not fantastic too. Their free cash flow isn't exactly very stable, and most years are just negative. I suppose they will have to continue borrowing from Peter to pay Paul.

Existing Hyflux 6% CPS

Throughout their listing, the hyflux 6% retail preference shares had never once dipped below its par value of $100. May 2011 to the present time isn't exactly kind to the stock market, so having maintained its share price above par is a great comfort to its holders. It acts as a good place to store their cash - it's a good cash equivalent that pays 6% pa, if you want to see it that way.

Their terms is 6% pa, payable semi annually on 25th April and 25th Oct every year, with first redemption on 25th April 2018. Thereafter, they will step up the rate from 6% to 8% if they don't redeem back.

Based on current price of 102.2, the yield to maturity until first redemption date is about 5.8%. Maybe by then, Hyflux will issue another preference shares, either institutional or retail, to roll over the debt. Considering that their pref shares at this kind of environment is still 6%, I think it'll be cheaper than to pay a higher stepped up rate of 8%. Maybe that's why the price of the pref shares is dropping steadily to par value. We're about 2 yrs shy of that first (optional) redemption date.

Note that the price shot up 3% on the first day, and thereafter within 2 months, shot up to about 7%. Not too shabby for a pref shares with 6% yield.

Conclusion

In summary, weak company but strong pref shares and dividend paying record. But that's all in the past, will it continue in the future? I think so and the gameplan, like Oxley and Perennial, is to continue issuing such bonds in the future. This should be quite a hot issue, I suspect. Actually, anything that is higher than fixed deposit rate is hot in Singapore these days, lol

Good for a stag. I'll expect it to be very hot.