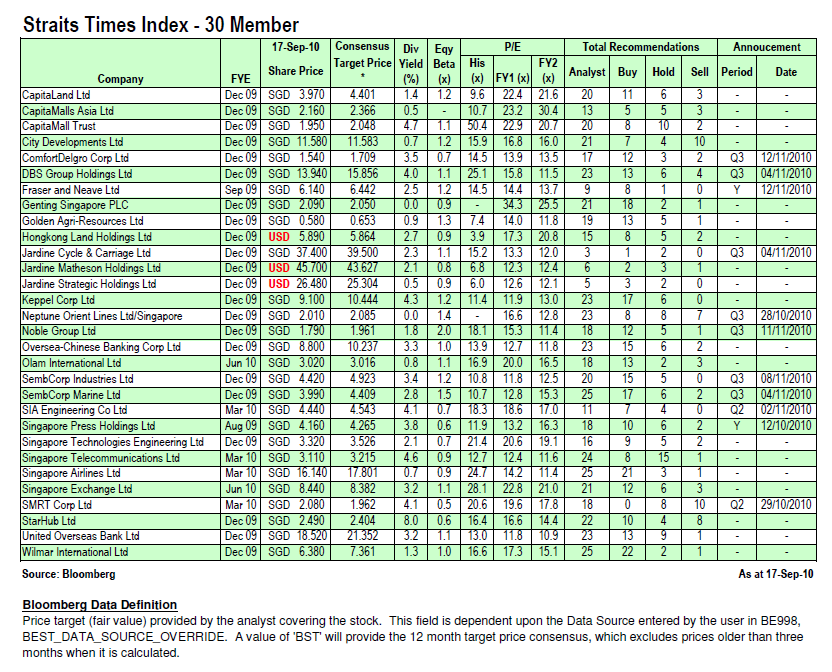

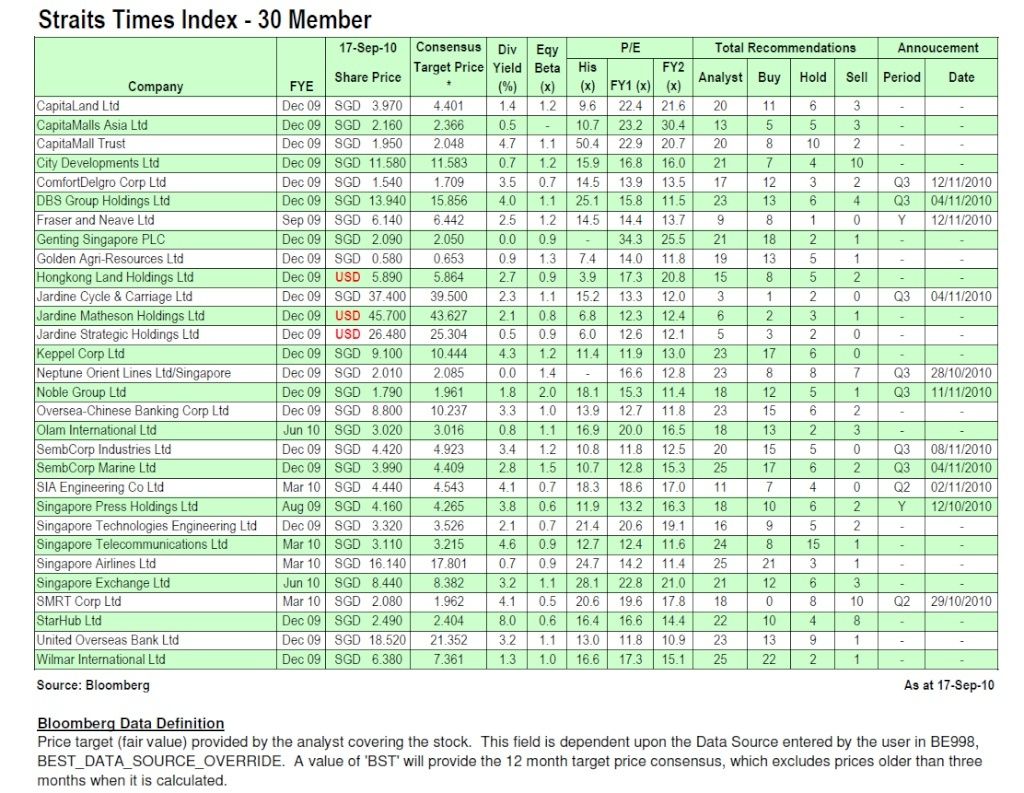

This is what I've observed about the data:

1. Just a quick look at the recommendations offered by analyst for the 30 counters, we can see that there is a heavy bias towards a buy call. With the exception of SMRT (0 Buy, 8 Holds, 10 Sells), you can see that most of the calls made by analyst are Buy calls. Seems like many are optimistic about the next one year ahead, with upgrading of earnings and the economy recovered from the last crisis. For analyst to stake a sell call is a heavy bet on their analyst and their reputation, so SMRT might be interesting to look at. Why is there so many analyst calling for a hold/sell and nothing on buy?

2. If you look at the consensus target price for the various counters, you'll notice that some had been reached, some had been exceeded and there are some marching towards their target price. The difference between the target price and the current price is not very far. If one is so inclined, I suppose the consensus estimate for STI for the next 1 yr can be computed by finding out the respective weightings for each counter. I'll just take the banks as a guide, knowing that they will form a big part of the weightings. I think another 10-15% in STI is expected. This means we're looking at around 3400 to 3600 in a year's time.

3. Looking at the PE ratio, you can see that the 'land' counters are really high compared to historical PE. Most of the other component stocks have their PE ratio in line with historical PE. Banks seems to be underperforming, with their historical PE higher than current. I believed that if STI is to go up higher, banks will be the one to catch up to bring the whole index upwards. For property counters, the direction seems clear - sideway (best scenario) or down (likely scenario). I think STI also seems to be sustainable at this level because except for the 'land' counters, the PE is not exceeding high above its historical PE. In fact, it's pretty much in line with it.

4. I didn't know that with the exception of Genting (perhaps it's new) and NOL (years of losses), the rest of the components stocks pay dividend. It'll be great to hold the bluest of the blue chip with a good dividend, but how to do that? We must be courageous and buy them when everybody wants to dump them. That's what we're here for right? To encourage each other to buy when others are fleeing, and to have a community to provide each other with the social proof of being greedy and others are fearful.

{kind=link}

2 comments :

Hi LP

SMRT is still a "safe" bet if the Govt's "target" of 7.5m residents is on track. How else can the masses move from point A to B?

I am also eyeing banking counters as an alternative for pathetic interest on savings and fixed deposits.

Be well and prosper.

Hi PG,

I think SMRT is a safe bet too, though perhaps not at this price, haha :) The chart shows the way to buy in or sell out :)

As for banking, my simplistic sense of how things work tells me that once interest rates rise up, they might make get better profits from the interest difference, so it should be a good bet. I'm already heavily into banks stocks, though not the local ones, haha

Post a Comment