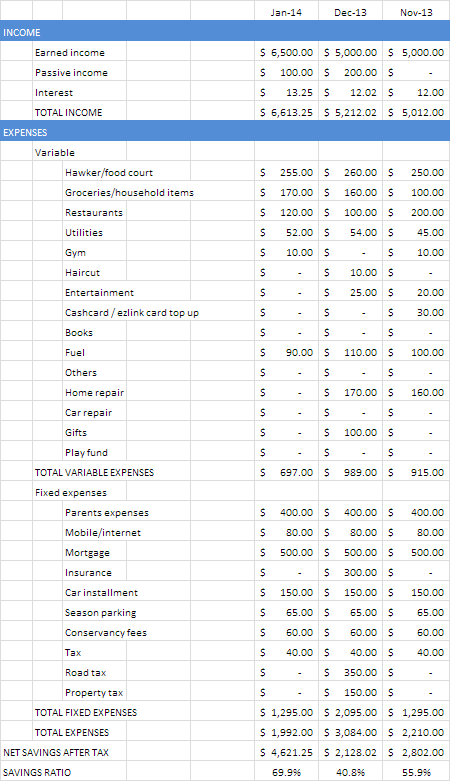

Seems like there's a lot more to say about the DBS 4.7% preference shares redemption.

I've been a little unfair to DBS on this previous post here. From well informed friends (thanks cory and pero), I learnt that DBS actually exchange that preference shares with another one with higher payout and shorter tenor around Nov 2013. This is done because the older preference shares no longer qualify as Tier 1 capital under the new Basel III capital adequacy requirements implemented by MAS on Jan 2013.

I cut and paste the notice here, for future reference:

-----------------------------------------------------------------------------------------------------

I've been a little unfair to DBS on this previous post here. From well informed friends (thanks cory and pero), I learnt that DBS actually exchange that preference shares with another one with higher payout and shorter tenor around Nov 2013. This is done because the older preference shares no longer qualify as Tier 1 capital under the new Basel III capital adequacy requirements implemented by MAS on Jan 2013.

I cut and paste the notice here, for future reference:

-----------------------------------------------------------------------------------------------------

DBS offers to trade new notes for $800m in preference shares

By Siow Li Sen lisen@sph.com.sg

Nov. 8 (Business Times) -- [SINGAPORE] DBS Group Holdings is

offering to buy back $800 million of an outstanding $1.7 billion preference

share issue, offering in exchange new notes with a higher payout and a shorter

tenor.

Existing note holders can, via a tender, exchange at par for

the new notes which will pay out 4.7-4.9 per cent, and has a call date in

November 2019, the bank said yesterday.

The callable date for the existing preference shares is 2020.

The non-cumulative non-convertible non-voting class N preference shares have a

payout of 4.7 per cent.

The reason for the bank's action is that the new shares will

be Basel III compliant and qualify as Tier 1 capital.

DBS said that "the fact that the existing preference

shares no longer fully qualify as Tier I capital of DBS Bank constitutes a

preference share change of qualification event" under the Basel III

capital adequacy requirements implemented by the Monetary Authority of

Singapore (MAS) on Jan 1, 2013.

In a statement yesterday, DBS said that it was

"proposing to accept tenders amounting to $800,000,000 in liquidation preference

of existing preference shares, or a lower or greater aggregate amount at (its)

discretion".

Holders who wish to participate must do so by 5pm Singapore time

on Nov 21, 2013.

The tender does not apply to the retail tranche issued also in

2010 - an $800 million 4.7 per cent non-cumulative non-convertible non-voting

class O preference shares callable in November 2020.

"We are starting with the institutional tranche - to

see market reaction," said a bank spokesman.

If the response is "overwhelming", a bigger issue

of the new notes could be considered, said Clifford Lee, DBS Bank head of fixed

income.

The 4.7-4.9 per cent payout and shorter tenor of the new preference

shares are seen as "investor friendly" and attractive relative to a

recent perpetual issue by United Overseas Bank (UOB).

In July, UOB sold $850 million of perpetual notes paying 4.9

per cent that were Basel III compliant. Yesterday, the notes were quoted at

$102.35-$102.85, yielding 4.335-4.219 per cent.

"Instead of a price nearer to 4.2 per cent, they're

(DBS) paying 4.7-4.9," said a banking source.

Still, some investors sold off the existing DBS preference shares

after the announcement, causing prices to fall to $100.51-$101.398 from $102.52

on Wednesday. They could be only looking at the exchange at par, and not the

coupon of the new bonds, suggested the source.

Said Gary Dugan, Coutts chief investment officer for Asia and

Middle East: "Anything (bank perpetuals) above 4 per cent is attractive."

Interest rates are likely to remain low for the next 2-3 years

and perpetuals still remain very attractive, he added.

Under MAS Notice 637, effective on Jan 1, 2013, Tier 1 securities

have a point of non-viability (PONV) loss-absorbing feature. What this means is

that investors or debt-holders will have to face a partial principal writedown

or conversion into common equity when the PONV is being triggered by MAS. The

PONV is triggered when MAS decides that a bank is no longer viable, or when

public-sector support is required.

Separately, a UOB spokeswoman said that the bank would not comment

on future capital management plans, when asked if it might consider similar

exchanges for its non-Basel compliant preference shares.

At OCBC Bank, Ang Suat Ching, its head of funding and capital

management, said that "while our existing preference shares are not Basel

III compliant, they will continue to qualify substantially as additional Tier 1

capital over the next few years under MAS's transitional Basel III rules".

"Our Tier 1 capital adequacy ratio as at end-September

was 14.3 per cent, a level that we are comfortable with. We continuously assess

our capital and financial requirements, as well as market conditions, in

determining any early redemption or new issuances of capital instruments."

Copyright 2013 Singapore Press Holdings

-0- Nov/08/2013 00:30 GMT

-------------------------------------------------------------------------------------------------

But there's still a bit of problem here:

1. Okay, totally understand that they have to do some engineering to change the structure of the preference shares to fit the ever stricter capital adequacy requirements. But $1.7 billion worth of existing preference shares are exchanged for $800 million worth of new ones. That's less than 50% of the existing shares offered to be exchanged. Exchange seems too strong a word. The proper wording should be "offer to exchange by balloting" because not all who wants to exchange it will get it, from the mere fact that there are lesser new issues than the one to be replaced. For those who had exchanged for the newer shares, good for them. For those who didn't got it, they are now redeemed based on the latest announcement by DBS on 13-Feb-2014.

2. The existing preference shares has a coupon yield of 4.7% pa. The newer one to be exchanged range from 4.7 to 4.9%. The range, I suppose, is dependent on how oversubscribed the new issues are. If there's $1.7 billion of preference shares being cut to $800 million worth, and they are all going to ballot for this newer issues with yield ranging from 4.7 to 4.9, it's not going to take much of a guess where the yield of the new issues will fall. With hindsight, we know that it's indeed 4.7% also. So, that doesn't really qualify as 'a higher payout', to quote the above announcement. If anything, it's "potentially higher payout".

But again, to be fair to DBS, they could have put the yield lower even than 4.7% and nobody can say anything.

Ultimately what am I going to do with the listed DBS 4.7% preference shares that I hold for my parent's account? I'm going to sit tight and do nothing. If it falls really close to par value, I might even add in some. What can happen? If they are going to redeem the listed DBS 4.7%, then they are going to offer new ones in exchange for it. They could go all bastard and reduce the total amount from the existing $800 million worth to something lesser, so all the holders will have to go ballot again for the new exchanged issues. Since I bought it at above par, I'll lose some capital but in exchange I can get newly issued ones at par, which is a good thing for me so that I can properly allocate my resources because of more certainty. I've already accounted for the potential loss in buying a pref shares above par value, so taking the loss wouldn't affect much in terms of the yield I promised to my parents. But a loss is still a loss, so it'll mean I have less buffer for other such things that can be thrown to me as my parent's fund manager.

But again, to be fair to DBS, they could have put the yield lower even than 4.7% and nobody can say anything.

Ultimately what am I going to do with the listed DBS 4.7% preference shares that I hold for my parent's account? I'm going to sit tight and do nothing. If it falls really close to par value, I might even add in some. What can happen? If they are going to redeem the listed DBS 4.7%, then they are going to offer new ones in exchange for it. They could go all bastard and reduce the total amount from the existing $800 million worth to something lesser, so all the holders will have to go ballot again for the new exchanged issues. Since I bought it at above par, I'll lose some capital but in exchange I can get newly issued ones at par, which is a good thing for me so that I can properly allocate my resources because of more certainty. I've already accounted for the potential loss in buying a pref shares above par value, so taking the loss wouldn't affect much in terms of the yield I promised to my parents. But a loss is still a loss, so it'll mean I have less buffer for other such things that can be thrown to me as my parent's fund manager.

.jpg)