This is an unpaid review of You Need A Budget, also known as YNAB. I bought it last month from steam at a discount, but had long heard of it by others who gave rave reviews about this personal finance software. Since it's at a great discount of 75%, I decided to plunge into it and try it for myself. Prior to this leap in using the software, I already had a working excel spreadsheet that works for me for the past 5 or so years. The spreadsheet is meant to keep tabs on my expenses and also keep records of all my transactions in the form of a cash flow statement, balance sheet and an income statement. I record all my expenses and the income flowing from my handphone using just a simple note taker, afterwhich I'll transfer the information to my spreadsheet in my computer after forthnightly or weekly.

As you can see, I'm not so hot about changing a system that works for me and that I'm so comfortable in using. But there's a few things about my system that I don't like. Firstly, it's hard to reconcile bank statements. Secondly, it's lacking a graphical interface. Call me shallow, but between a system that works 100% but is ugly and a system that works 90% but is pretty, I'll go for the second one. The nice interface makes me want to do this forever, not that I'm lacking in motivation.

YNAB is basically a budgeting software. You decide, at the start of the month, how much each dollar you would give to different envelopes, like food, entertainment, handphone bills etc. They also have a free android app (I checked, they have an app for iOS as well) that ties in very nicely with the software that is installed on your main computer. The information between the app and the one in your computer can be synced using dropbox. All the backup and data are placed in the dropbox, so you can start your YNAB budget from one of these autosaved points, which can be very handy in case something horrible happened that wiped out all your hard work in keeping tabs on your personal finance.

I realized that I'm using this software less like a budgeting software, but more like an accounting software, where all my transactions between accounts and cashflow in and out of accounts are recorded and kept track of. I guess this would take some time to adjust because as mentioned, I've never done budgeting before and I already knew roughly what my expenses are for different categories. But I always say we can do better, that's why I did a system overhaul by adopting this new software.

One of the good things I like about YNAB is that because it's all programmed nicely, it's exceedingly easier to change things and make sure that everything is still tallied. During the past one month of using the software, I had to do some major changes to my account. In the past, using spreadsheet, I've to comb though the worksheets of the previous months carefully. But for now, I just have to key in the new changes, and everything else is taken care of. Needless to say, I'm suitably impressed. Though I'm not expecting much major changes going forward, it's still a nice feature to have knowing that any new way to partitioning your personal wealth is easily down with a click of a few buttons. Effortless.

I keyed in all my accounts in YNAB, including all the marked to market value of my various investment portfolio, insurance cash value, and all the shitloads of debts that I owed HDB. Straightway, I can see my networth displayed with superbly clean charts and nicely tabulated figures. If I need to see my income vs expenses, there's another tab to click to see it too. I can compare data across the years, the past 3 months, this month and the year to date. This is something that I can't do easily since I divided my expenses spreadsheet physically year by year. I can, of course, combine them, but again, it's the ease of use in YNAB that blows me off.

In summary, here's what I like about YNAB:

1. Extremely easy to check and reconcile accounts.

If your actual statements and the one you had in YNAB differs even by a cent, it'll alert you and you can do the necessary checking. Saves me a hell lot of time for this little function.

2. Very clean and nice graphical user interface

Clean and nice. The reports generated are also very good, if you're into this sort of thing. Makes you want to keep checking it.

3. Ability to change things easily and keeps backup on dropbox

If you make a fatal mistake, you can return to the last autosaved place. Changing something automatically changes everything from the past to this moment. You won't appreciate this until you got something major to change, so trust me on this one.

4. It has an well integrated free app on android.

I used to key my expenses into a simple note taker in my phone, then transfer the records over to my spreadsheet over at my computer. This doesn't take much time but it still takes some time. With this app, whatever I keyed into my hp automatically gets synced to the software at my main computer. That makes my life soooo much easier. Just this alone makes this software worth adopting.

5. Very nicely integrated philosophy behind the programming

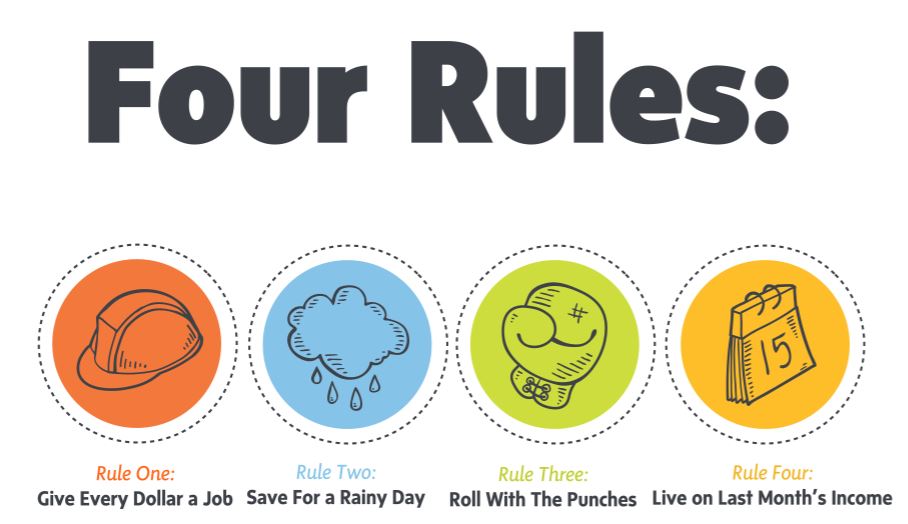

Once you start downloading the software, you'll be in a short but useful online lecture program on how to jumpstart your failing financial management knowledge. You'll be exposed to very good advice to save up, to do proper budgeting and basically good personal finance habits. Even I find it useful. I particularly like a phrase which they used very often - "Give every dollar a job!". If want to learn more, there's even free live classes that you can sign up and learn about various topics. It seems like the people behind YNAB is really interested in making you financial healthy. They are really serious in making you change your mindset to have real change in your life.

Here's what not to like about YNAB:

1. Poor integration of financial aspects

If you're looking for something that can keep track of your investments, this is not for you. It works very well in what it aims to do, and this is just not one of its function. I still using my trusty old spreadsheet for that purpose.

2. No auto download of credit card statements or bank statements

Actually maybe it does have but I don't like the idea of it at all. If you want to keep tabs on your expenses, then do so. The act of doing it will bring a lot of benefits rather than downloading the statements automatically from the bank. However, if you really want to, you can download credit or bank statements, then upload it to YNAB. It can accept .OFX , .QFX, .QIF and .CSV format. I wouldn't recommend it, neither do the people behind YNAB.

3. Tracks the amount of money right to the cent

What's not to like about this? Well, usually when I'm keeping tabs on expenses manually, I disregard anything less than $1. I also don't count the money that I've in my wallet. This program forces me to count each and every cent. There are many times that I noticed that the amount of money that I had and the amount of money that I'm supposed to have in my wallet do not tally. I need to reconcile the differences. This means I must have missed out some stuff...Not a big sum (<$15), but can be irritating when the software highlights to me that I missed something out and I'm the sort of person who then have to correct the mistakes. It's making me anal fussing over 10 cts here and 20 cts there. Granted, this is the point, afterall.

I really think this software is worth putting the time and effort to learn. For newbies who are starting out to earn their first drop of cash, it'll make you learn a few good habits that can last you for life. That alone is worth the price of this software. For those who had been tracking your expenses fastidiously all along using excel spreadsheet, perhaps a little more graphics, a little more automation can make an easy job even easier. Do try it as they have a full featured demo for 34 days - more than enough time for you to try it out to see if it can fit in to your life. No harm trying right?

As you can see, I'm not so hot about changing a system that works for me and that I'm so comfortable in using. But there's a few things about my system that I don't like. Firstly, it's hard to reconcile bank statements. Secondly, it's lacking a graphical interface. Call me shallow, but between a system that works 100% but is ugly and a system that works 90% but is pretty, I'll go for the second one. The nice interface makes me want to do this forever, not that I'm lacking in motivation.

YNAB is basically a budgeting software. You decide, at the start of the month, how much each dollar you would give to different envelopes, like food, entertainment, handphone bills etc. They also have a free android app (I checked, they have an app for iOS as well) that ties in very nicely with the software that is installed on your main computer. The information between the app and the one in your computer can be synced using dropbox. All the backup and data are placed in the dropbox, so you can start your YNAB budget from one of these autosaved points, which can be very handy in case something horrible happened that wiped out all your hard work in keeping tabs on your personal finance.

|

| Nice clean interface makes you want to key in something! |

I realized that I'm using this software less like a budgeting software, but more like an accounting software, where all my transactions between accounts and cashflow in and out of accounts are recorded and kept track of. I guess this would take some time to adjust because as mentioned, I've never done budgeting before and I already knew roughly what my expenses are for different categories. But I always say we can do better, that's why I did a system overhaul by adopting this new software.

One of the good things I like about YNAB is that because it's all programmed nicely, it's exceedingly easier to change things and make sure that everything is still tallied. During the past one month of using the software, I had to do some major changes to my account. In the past, using spreadsheet, I've to comb though the worksheets of the previous months carefully. But for now, I just have to key in the new changes, and everything else is taken care of. Needless to say, I'm suitably impressed. Though I'm not expecting much major changes going forward, it's still a nice feature to have knowing that any new way to partitioning your personal wealth is easily down with a click of a few buttons. Effortless.

|

| The YNAB app on mobile phones makes it very easy to key in transactions and it auto syncs. |

I keyed in all my accounts in YNAB, including all the marked to market value of my various investment portfolio, insurance cash value, and all the shitloads of debts that I owed HDB. Straightway, I can see my networth displayed with superbly clean charts and nicely tabulated figures. If I need to see my income vs expenses, there's another tab to click to see it too. I can compare data across the years, the past 3 months, this month and the year to date. This is something that I can't do easily since I divided my expenses spreadsheet physically year by year. I can, of course, combine them, but again, it's the ease of use in YNAB that blows me off.

|

| Nice pie chart showing you the different categories of expenses according to timeline that you set |

In summary, here's what I like about YNAB:

1. Extremely easy to check and reconcile accounts.

If your actual statements and the one you had in YNAB differs even by a cent, it'll alert you and you can do the necessary checking. Saves me a hell lot of time for this little function.

2. Very clean and nice graphical user interface

Clean and nice. The reports generated are also very good, if you're into this sort of thing. Makes you want to keep checking it.

3. Ability to change things easily and keeps backup on dropbox

If you make a fatal mistake, you can return to the last autosaved place. Changing something automatically changes everything from the past to this moment. You won't appreciate this until you got something major to change, so trust me on this one.

4. It has an well integrated free app on android.

I used to key my expenses into a simple note taker in my phone, then transfer the records over to my spreadsheet over at my computer. This doesn't take much time but it still takes some time. With this app, whatever I keyed into my hp automatically gets synced to the software at my main computer. That makes my life soooo much easier. Just this alone makes this software worth adopting.

5. Very nicely integrated philosophy behind the programming

Once you start downloading the software, you'll be in a short but useful online lecture program on how to jumpstart your failing financial management knowledge. You'll be exposed to very good advice to save up, to do proper budgeting and basically good personal finance habits. Even I find it useful. I particularly like a phrase which they used very often - "Give every dollar a job!". If want to learn more, there's even free live classes that you can sign up and learn about various topics. It seems like the people behind YNAB is really interested in making you financial healthy. They are really serious in making you change your mindset to have real change in your life.

|

| Rule number 1: Give every frakking dollar a job! |

Here's what not to like about YNAB:

1. Poor integration of financial aspects

If you're looking for something that can keep track of your investments, this is not for you. It works very well in what it aims to do, and this is just not one of its function. I still using my trusty old spreadsheet for that purpose.

2. No auto download of credit card statements or bank statements

Actually maybe it does have but I don't like the idea of it at all. If you want to keep tabs on your expenses, then do so. The act of doing it will bring a lot of benefits rather than downloading the statements automatically from the bank. However, if you really want to, you can download credit or bank statements, then upload it to YNAB. It can accept .OFX , .QFX, .QIF and .CSV format. I wouldn't recommend it, neither do the people behind YNAB.

3. Tracks the amount of money right to the cent

What's not to like about this? Well, usually when I'm keeping tabs on expenses manually, I disregard anything less than $1. I also don't count the money that I've in my wallet. This program forces me to count each and every cent. There are many times that I noticed that the amount of money that I had and the amount of money that I'm supposed to have in my wallet do not tally. I need to reconcile the differences. This means I must have missed out some stuff...Not a big sum (<$15), but can be irritating when the software highlights to me that I missed something out and I'm the sort of person who then have to correct the mistakes. It's making me anal fussing over 10 cts here and 20 cts there. Granted, this is the point, afterall.

I really think this software is worth putting the time and effort to learn. For newbies who are starting out to earn their first drop of cash, it'll make you learn a few good habits that can last you for life. That alone is worth the price of this software. For those who had been tracking your expenses fastidiously all along using excel spreadsheet, perhaps a little more graphics, a little more automation can make an easy job even easier. Do try it as they have a full featured demo for 34 days - more than enough time for you to try it out to see if it can fit in to your life. No harm trying right?