My aim is to invest the 50k for a min of 2% and above, with very good chances of not losing the capital. This is not a growth-dividend portfolio, because I'm guaranteeing the capital. This is also not a high dividend yield portfolio, because I don't need to take the necessary risk to get the 2%, and neither can I guarantee the capital if the market goes down. As such, I'm only putting the money into pref shares/bonds. I choose bonds because as long as I hold till maturity, the ups and down of the price wouldn't affect me. Pref shares because they have a very low volatility; even during the financial crisis, it dropped 20+% but recovered. Most of the time the share prices are range bound. I just need to worry about whether the underlying companies are steady enough and won't go bankrupt throughout the holding period, hence I only pick government-linked companies and banks. Especially banks lol

I've put the money into 4 counters with the respective % (included commission) in brackets:

1. CapMallA3.8%b220112 (10.3%)

2. DBS Bk 4.7% NCPS 100 (42.9%)

3. OCBC Bk 4.2% NCPS (24.6%)

4. OCC 5.1% NCPS 100 (21.3%)

5. Cash (0.8%)

Total: 100%

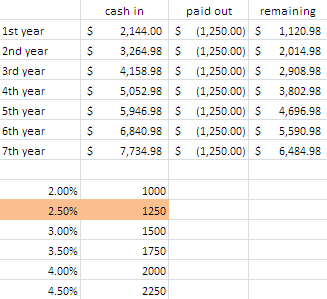

By allocating as such, I'll have a cash flow of $2,144 per year, which is equivalent to a 4.29% portfolio yield, inclusive of commission. I plan to give my parents 2.50% pa, keeping the remaining 1.79% to buffer against the loss of capital when the pref shares and bonds are redeemed at par value when they mature. With this spare cash accumulated over 2 years plus, I can also buffer against a drop in prices of around 10 to 15% (amounting to 2.3k to 4.8k), in case they want to get the money out before maturity and I have to sell below my buy price.

|

| Estimated cash flow. Things will be a bit hairy upon the 5,6 and 7th year as some will be matured. But no point thinking so far ahead. A step at a time. |

1. CapMallA3.8% (5 lots, board lot size 1000 shares)

This is the only bond that I have. The maturity date is 8.1 yrs from now, on 12-Jan-2022. There's optional redemption on 12-Jan-2017, 12-Jan-2018, 2019, 2020 and 2021. If they didn't redeem on 2017, then the interest will step up from 3.8% pa to 4.5% pa. It's a good thing if they redeem early, because by then, the higher interest rate environment might offer me more choices of bonds/pref shares that pay a higher yield too. If they don't redeem, I'll get a stepped up interest of 4.5% pa, so it's good too. Capmallasia is just more risky as a company compared to banks, so I only allocate 10% of the portfolio to it.

Do take note that if you buy now, you won't be in time to get the payment on Jan because the counter just went XI. The price, however, also dropped, so the total returns will be a little different from what I've put up in previous posts.

2. DBS 4.7% NCPS (2 lots, board lot size 100 shares)

They can first redeem on 22nd Nov 2020, which is 6.9 yrs from now, but this is an option for the issuers, not a requirement. You'll get 4.7% pa flat while holding.

3. OCBC 4.2% (12 lots, board lot size 1000 shares)

For this one, it's the more risky of the pref shares that I had bought. This is because the optional redemption date is on 14th July 2013, which had long passed. They can have the option to redeem anytime when they give the payments on 4th Jun and 4th Dec every year. Since I bought it above par, if they decide to redeem on the 4th June this year, which is one of their payment dates, I'll lose money. Based on my entry of 1.025, I just need to get 1 full year of interest at $0.042 and I'll be safe. That said, I think the chances of them redeeming on this kind of environment is going to be low. If anything, they shouldn't redeem this. They had already redeemed the higher interest bearing pref shares, so this is one of the lower one. It's a good bet, I think.

4. OCC 5.1% (1 lot, board lot size 100 shares)

For this, there's two interest rate. Before the first optional redemption on 20th Sept 2018 (4.7 yrs from now), the interest is 5.1%, based on $100 share price. If they did not redeem on that date, the interest will be 2.5% + 3mth SOR. Currently, the 3mth SOR is about 0.2 %, and 4.7 yrs from now, it should increase, not decrease. Since I'm happy getting a minimum of 2.5 % + 0.2% = 2.7 % pa, I got this too.

25 comments :

LP,

Interesting.

You have become the CPF board to your parents ;)

Hi SMOL,

Haha, indeed, now I'm the guardian of the money and I'll have to make sure it's safe..it's quite different from managing my own money really :)

by managing other people money, when it comes from people u know especially ur parents, do u handle it with much more care than your usual portfolio?

HA! Ha!

i did it differently when i managed my MIL's 15K, deposited with my wife.

My MIL just expect bank's FD rate of returns.

i told my wife i would invest the 15K in equities in the market@dividend yields of at least 3 to 5 %. with 100% guaranteed of capital.

But any capital gain or lost in the investment would be mine.

In other words, my MIL's 15K is treated as treasury Bond@ 3% to 5% or higher yield, as far she is concerned. She could withdraw her fund at anytime.

After about 2 years she claimed back her money with about 1200 dollars or more paid up as interest. As she needed the money than.

Might as well. But i did have a little capital gain.

i admit i dared to do it this way because i can afford the risk. And only for my MIL.

Managing someone else money is never easy, esp. if it is a blood relation.

Btw, there cannot be a formal or legal contract for managing other peoples money unless you are a MAS licensed fund manager or equivalent.

This offence is jail-able if found out as shown by one of the training school founder.

Hi LP,

For DBS 4.7% NCPS, would it be correct to say that an investor buying in at the current price of 107.45 will need to wait for at least 2 annual paymets of 9.4% to achieve a positive return?

Hi anonymous,

Yes, I have to take into consideration their investment horizons in my portfolio allocation, so that if they want to withdraw partially, I can take it out without affecting the cashflow that much. I also have to look carefully at the riskiness of the yield.

It dawned on me that I treat other people's money more carefully than my own. I should bear that in mind in the future when I'm investing my own money :)

Hi temperament,

Wow, that's like 4% pa returns :) Your fund is about the same as mine, guaranteed capital with a fixed returns too :)

Exactly, it's only for your close relations...any other people would be charged a 'management fees' lol

Hi numbers,

I think the licensing is only for those with more than 30 qualified investors. Most fund managers in singapore, at least those boutique ones, should fall out of these category I guess :)

Hi Nickguthe,

Yup, that's right. Specifically, because they pay semi-annually at 2.35%, you would need to get 4 such payments to break even, assuming that the share price don't rise up too. I think the risk are higher if they can opt to redeem within the next 2 years, otherwise, holding this longer will make it safer in terms of recovery of capital.

If it is too good to be true, then it is probably risky.

Better to be low risk investment for the elderly (unless the relative takes on the risk on behalf and guarantees the capital and returns to the elderly)

Hi LP,

That's a very sensible approach and a pretty conservative portfolio. I think you did a great job!

I invested my mum's money into CLOB shares when I was 21 or 22 years old and she never saw her money again! :P

I wasn't sure it was my ignorance, risk appetite, or my conceit that killed her investments. Anyhow, I was guilty as charged.

With the responsibility, comes the pressure/stress.

It's never easy managing family money. Money can topple even the tightest kinship.

Anyway, try not to buy bonds above par next time.

And do prepare your plan on what to do next. Ie, what is the implication of an interest rate rise and how you have to re-allocate the portfolio(and whether there is capital risk).

Imagine this, if interest rate ever goes up to 3-4%, FD rates might also go up likewise. So why should your parent put the money with you when they can get 4% risk-free with deposit. So you might then need to offer a higher rate to retain them.

Hi EY,

Oh, you didn't! Wow, I wonder how they are going to trust you with money next time lol

Whether it's a good and conservative portfolio, I think only time will tell ;) Maybe next time they will swear me off from touching their money again in the future lol

Keeping fingers crossed :)

Hi WJ,

Long time no see :)

Is there any reason why you don't recommend buying bonds above par, beyond the fact that there'll be a capital loss when it's redeemed? I think if that capital loss is incorporated in the investment thesis, then it's like buying a bond at par but with lower yield. Shouldn't make any difference as long as you hold to maturity, should it?

Yup, thanks for your advice on the preparation of a plan in the future. I had one thought out already. When the interest rate rise, the price of the bonds/pref shares will likely fall. But I'm not going to sell it and will hold until they are redeemed. Hence, the price fluctuations doesn't really concern me.

If my parents want to take out the money before redemption, I'll 'buy' the portfolio over from them , return them their capital and take over the portfolio. But there's still some reserve cash that is not distributed to them (i can get 4.3% but distributing only 2.5%), so I get to keep them to lower down my cost of taking over their portfolio.

If they didn't take out the money prematurely, and the bonds are redeemed by the issuer, I'll not only return them their capital and will also include a nice big bonus of whatever retained cash over the years.

If the interest rate rises to 3-4%, and the fd rates went up, and they choose to park it with the banks, I'm more than happy to return them their capital and wash my hands off this matter. I'm not looking to retain them at all if they can find a safe and good returns. To be honest, there's no incentives at all to help them (I can think of many disincentives though) except that I don't want to see them taking lousy 1+% pa with time deposits now, haha!

hi lp. can you share the yield per instrument?

coco

Hi coco,

I've done a series of posts before this one, that highlights the different yields and dates of maturity plus other fine prints. It's listed here:

1. http://bullythebear.blogspot.sg/2013/12/retail-bonds-listed-in-sgx.html

2. http://bullythebear.blogspot.sg/2013/12/preference-shares-listed-on-sgx.html

3. http://bullythebear.blogspot.sg/2013/12/sg-bonds-listed-in-sgx.html

It's all listed out there together, and you should read the yields with the fineprints that comes along with it, because some of them involve different yields at different dates.

Let me know if you've any more queries. Will be happy to help.

LP,

Congrats on constructing a great passive income portfolio.

To further improve it, I would recommend you explore leveraging on the fixed income instruments to buy even more.

Regards,

Newbie

Hi Newbie,

Hey, long time no see! Ya, I still remembered the conversation in the cbox that we had long ago regarding this. I'll look into this, but I won't do it for my parent's portfolio lol

Hi LP,

Thank you for sharing your parent's portfolio with us! Just wondering whether do you consider to add STI ETF into your parent's portfolio? If not, may I know why not?

Thank you for your reply.

Cheers,

Ryan

Hi Ryan,

Nope, I don't intend to add STI etf. The reason is that the investment horizon for STI should be in tens of years, not less than ten years (which is the max my parent's investment horizon should be). As my parent's investment fund is mainly for the dividends, not for capital gains, investing in STI etf doesn't suit my purpose. Even though there is about 3% yield pa for the STI etf, there is also the possibility of losses unlike holding bonds/pref shares till redemption. I did a research that shows that you might need to hold about 14-15 yrs for STI before it can return give you a non zero returns for the holding period - so, I better not risk it because I'm the one guaranteeing any losses!

However, if your investment horizon is more than 10 years and the purpose is for capital gains, that might be a good idea. Then I probably also won't put the bulk of the fund in fixed income :)

For the next tranche of money that I might help my parents to invest, I might help them do a fund that focuses more on capital appreciation. But I can't guarantee anything! LOL

www.stokflok.com/content/retail-bonds-listed-sgx

Hi anonymous,

Why are you pasting a link here?

Hello Everybody,

My name is Mrs Sharon Sim. I live in Singapore and i am a happy woman today? and i told my self that any lender that rescue my family from our poor situation, i will refer any person that is looking for loan to him, he gave me happiness to me and my family, i was in need of a loan of S$250,000.00 to start my life all over as i am a single mother with 3 kids I met this honest and GOD fearing man loan lender that help me with a loan of S$250,000.00 SG. Dollar, he is a GOD fearing man, if you are in need of loan and you will pay back the loan please contact him tell him that is Mrs Sharon, that refer you to him. contact Dr Purva Pius,via email:(urgentloan22@gmail.com) Thank you.

BORROWERS APPLICATION DETAILS

1. Name Of Applicant in Full:……..

2. Telephone Numbers:……….

3. Address and Location:…….

4. Amount in request………..

5. Repayment Period:………..

6. Purpose Of Loan………….

7. country…………………

8. phone…………………..

9. occupation………………

10.age/sex…………………

11.Monthly Income…………..

12.Email……………..

Regards.

Managements

Email Kindly Contact: urgentloan22@gmail.com

Post a Comment