Terms of the security

The terms of the perps is spelled out very clearly in the announcement here:

1. Public offer of up to 230 million (can go up to 250 million), out of total size of 300 million (can go up to 500 million) if oversubscribed

2. Opens on 18th May, close on 25th May noon

3. Min amount is $2k, thereafter in multiples of $1k.

4. This is the interesting feature about the issue. They are giving 6% pa, paid semi-annually (on 27th May and 27th Nov every yr) for first 4 yrs until and excluding 27th May 2020. From 27th May 2020 (inclusive), it'll not be 6% pa anymore, but will be at reset distribution rate.

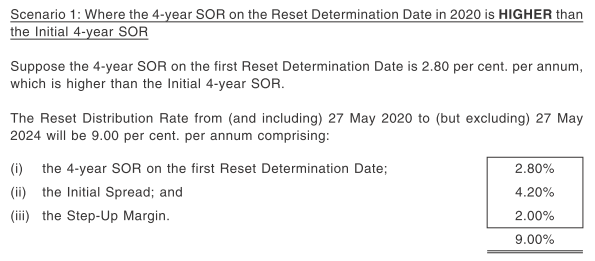

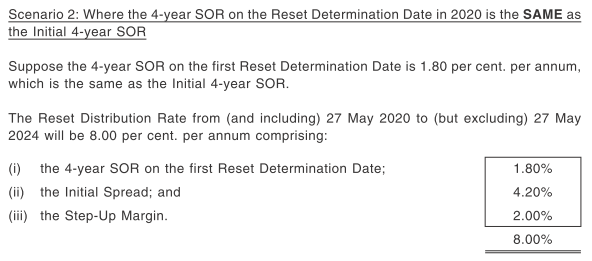

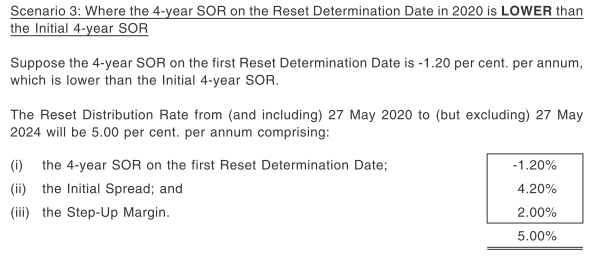

Reset distribution rate = 4 yr SOR on the reset date + 4.2% pa, + step up margin of 2% pa

They gave excellent illustration for 3 different scenario after 2020 to 2024, shown below:

5. From 2024 onwards, the distribution will be reset again using the formula shown in point 3, but with a new 4 year SOR rate at the reset date in 2024.

a. A dividend is paid to its junior obligations. I take junior obligations as the ordinary shares of Hyflux. I may be wrong.

b. If the junior obligation is redeemed, reduced, cancelled or bought back.

This means that if they give out dividends in their junior obligations (I take it as the ordinary shares of Hyflux, which I may be wrong), and/or they did not redeem, cancel or bought back all the junior obligations in a period of 6 months before the distribution payment date, they cannot defer distribution to this security.

Don't ever think they are obligated to pay holders of this security. You have a right to receive but they are not obligated to do so under the stated conditions. But it's not as bad.

They have a feature in this issue that is quite similar to any cumulative pref shares or bond. If they did not pay out any distribution in full or in part, that portion that is not paid out will be placed under arrears of distribution. They will have to pay out the arrears, plus any distribution, by the time they redeem back the securities, or by the next distribution payment date, or before they wind up, whichever comes earlier. If not, they cannot declare or pay dividends to its junior obligations or to redeem, back buy, cancel, reduce it.

I think in simple layman's language, it just means that they must pay out the dividends on the distribution date, unless they are also not giving dividends to hyflux ordinary shares/bond/pref shares holders. That is your sort of guarantee that they will pay out what they should pay out.

7. First redeemable date is on 27th May 2020, which is about 4 years from now, at the par value. They have to redeem all the outstanding amount or none at all. Thereafter, on each distribution payment date, meaning 27th May or 27th Nov after May 2020, they have an option to redeem back too. As mentioned earlier, this is a perp, so there is no fixed maturity date.

Financial strength of Hyflux

Alright, so far that's just the details of the perp. It's quite a complex issue, if you ask me. My initial excitement becomes a lot more muted once I took a look at Hyflux results.

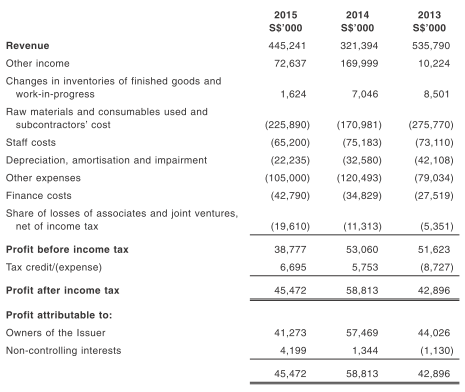

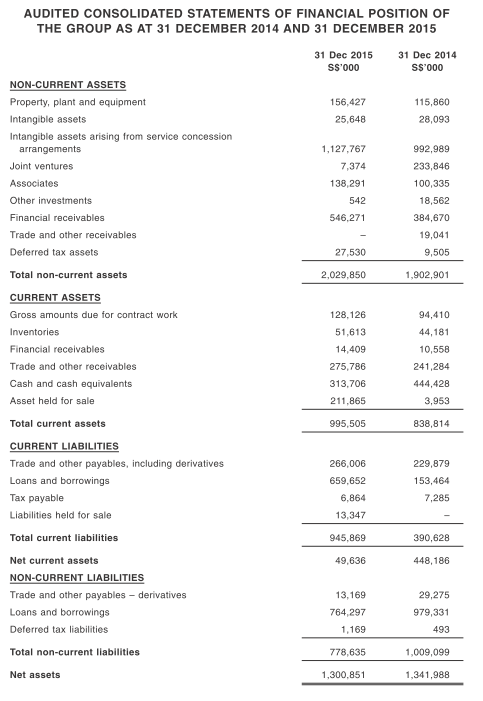

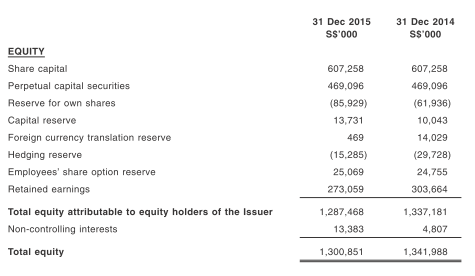

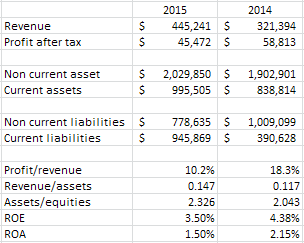

I'm too lazy to dig out past 10 yrs of financial statements, so using the last 2 yrs should suffice:

With a ROE of 3.5% in 2015, this isn't a company that I would have invested. But the pref or bonds issued might be a different story. Are they highly leveraged? Below is the ROE for Oxley. They also recently issued a new bond less than a year after their had their first retail one.

Looking at their financial leverage (Assets/equities), Oxley is the more leveraged one, but they are different industry of course. There really isn't a direct comparison for Hyflux. The question is, can they survive for 4 years or more and continue giving dividends to their ordinary shares as well as their bond/perps holders? I'm not confident. Revenue is contract and order based, so a bit lumpy. Even with their leverage, their ROE is not fantastic too. Their free cash flow isn't exactly very stable, and most years are just negative. I suppose they will have to continue borrowing from Peter to pay Paul.

Existing Hyflux 6% CPS

Throughout their listing, the hyflux 6% retail preference shares had never once dipped below its par value of $100. May 2011 to the present time isn't exactly kind to the stock market, so having maintained its share price above par is a great comfort to its holders. It acts as a good place to store their cash - it's a good cash equivalent that pays 6% pa, if you want to see it that way.

Their terms is 6% pa, payable semi annually on 25th April and 25th Oct every year, with first redemption on 25th April 2018. Thereafter, they will step up the rate from 6% to 8% if they don't redeem back.

Based on current price of 102.2, the yield to maturity until first redemption date is about 5.8%. Maybe by then, Hyflux will issue another preference shares, either institutional or retail, to roll over the debt. Considering that their pref shares at this kind of environment is still 6%, I think it'll be cheaper than to pay a higher stepped up rate of 8%. Maybe that's why the price of the pref shares is dropping steadily to par value. We're about 2 yrs shy of that first (optional) redemption date.

Note that the price shot up 3% on the first day, and thereafter within 2 months, shot up to about 7%. Not too shabby for a pref shares with 6% yield.

Conclusion

In summary, weak company but strong pref shares and dividend paying record. But that's all in the past, will it continue in the future? I think so and the gameplan, like Oxley and Perennial, is to continue issuing such bonds in the future. This should be quite a hot issue, I suspect. Actually, anything that is higher than fixed deposit rate is hot in Singapore these days, lol

Good for a stag. I'll expect it to be very hot.

34 comments :

Is the probability of 4 yr SOR goes negative high?

Hi starlight,

I'll say it's unlikely. Here's the historical SOR rate - "http://www.mortgagesupermart.com.sg/resources/sibor-sor-rates"

It went down really low but never dipped below 0% since 2004. Should be safe to say that the chances are really low. Of course, past don't ever predict the future. I think the chances of them redeeming back before the re-rating is higher haha!

Sorry noob here. How do I buy the mentioned hyflux perpetual?

Hi anonymous,

You can subscribe for it thru internet or ATM machine. Below are the instructions for POSB/DBS atm:

1 : Insert your personal DBS Bank or POSB ATM Card.

2 : Enter your Personal Identification Number.

3 : Select “MORE SERVICES”.

4 : Select language (for customers using multi-language card).

5 : Select “ESA-IPO/RIGHT APPLN/BONDS/SSB/SGS/INVESTMENTS”.

6 : Select “ELECTRONIC SECURITY APPLN (IPOS/BOND/SECURITIES)”.

7 : Read and understand the following statements which will appear on the screen.

8 : Select “HYF_PERP” to display details in relation to the Securities.

9: Press the “ENTER” key to acknowledge:

10 : Select your nationality.

11. Select your payment method.

12. Select the DBS Bank account (Autosave/Current/Savings/Savings Plus) or the POSB

account (Current/Savings) from which to debit your application moneys.

13. Enter the number of securities you wish to apply for using cash.

14. Enter or confirm (if your CDP Securities Account number has already been stored in

DBS Bank’s records) your own 12-digit CDP Securities Account number (Note: This

step will be omitted automatically if your Securities Account Number has already been

stored in DBS Bank’s records).

15. Check the details of your securities application, your CDP Securities Account number,

the principal amount of Securities applied and application amount on the screen and

press the “ENTER” key to confirm your application.

16. Remove the ATM Transaction Record for your reference and retention only.

Tks LP for replying my query

Hi LP,

If it is business as usual, all will survive. Just issue more to redeem old. Only when there is a credit event will those "swimming naked" be it trouble. Gahment will most properly help in rights if situation get really bad, it seems to me Hyflux is doing more "national services"

Then trying to be profitable. (Compare it with sembcorp with also a water treatment arm)

But if I remember correctly.

Dividends or interest must be given in this order:

Bonds first

Preference shares

Lastly common shares

Default on bond payment is a credit event; preferences shares are not

Pretty scary if u ask me; while I dun believe China credit binge will blow, the world

Is on a monetary binge

Does 6%pa reasonable to justify for the associated risks? Thank you.

I think the current retail bonds on SGX even by the bigger names like Frasers and Capmall have come down due to the expectation of higher interest rates. Wonder if perps would react the same although I know it is accounted as equity? If so, then that is an additional risk.

Are we talking about 4-year SOR? Where can we find the source?

Hi SI,

You're right. If things go smoothly, everyone is happy and good. It's only when times are bad and credit dries up, you'll see who is really swimming in mountain of debts.

Bond must make payment, if not it'll severely affect their ability to borrow money from banks next time. But pref shares, haha, like you've said, is like companies not declaring dividends. No big deal haha

Hi starlight,

I've no idea. That is for you to do your own risk assessment. Just know what you're getting into if you choose to subscribe and put in the right amount to limit the downside. Don't treat this as a safe fixed D with 6% pa returns.

Hi gnooliew,

I think it will come down too. In all purpose, pref shares is like a bond. I think the key idea is to be able to hold on to this till redeem it back. If not, like bond, you'll take the price risk that it might go below par value. If you're holding to maturity, even though we don't know when it will be, the price volatility wouldn't concern you.

Hi PH,

Yes, 4 yr SOR. Good question on where to find it. So far, I've not found 4 yr SOR rate, 1,3,6,12 months SOR. But the longer the year, the higher the SOR I suppose, so 4 yr SOR will be higher than 1 yr SOR. How high? I've no idea.

Hi do you know how to apply through a UOB ATM? I tried but it didnt seem to appear...sorry noob here too

Hi anonymous,

You can't do it through UOB. Have to be OCBC or DBS. You can do it online through internet banking too, so you don't even have to queue at ATM.

Hi, can I sell the pre bond within the 4 years or after? And how to sell - just like selling stock in SGX? Thks for any reply

Hi anonymous,

Yes, you can sell it anytime. It's just like any stocks listed in sgx, but since you didn't wait until they redeemed, you'll be selling at market price. If they redeemed it back from you, they will always buy back from you at $1, regardless of market price, and without comms.

Is it a must that they buy back from you at minimum $1?

Yes, that's the par value of the bond, unless I misread the value. They will always redeem back at par regardless.

6% pa, paid semi-annually, starts from 27th May 2016?

Ignore pls, found the answer:

The first payment of distributions scheduled to be made on Nov 27, 2016.

"DISTRIBUTION DEFERRAL: At issuer's discretion. Any deferred distributions are cumulative and on a compounding basis"

correct my understanding..

if missed payout for one semi-annual distribution, it will accumlate to the next payout?

and if they miss the payout, they will not distribute to their shareholders?

the risk to the perp holders seem very minimised.

even with SOR 0%, it is pretty much a guaranteed 6% yield.

only downside is the the bond falls below par value.

seems like too good to be true?

sorry, but what does it mean , by "stag"?

Hi foolish chameleon,

Actually you can see it the other way too - why make it cumulative? It could be to entice people to take it up too. In either case, I see the 'guarantee' as a promise that need not have to be fulfilled. If the situation is so bad that they can't pay out a dividend, then it can't pay out a dividend. If it can't pay this year, it's even harder to pay the following year, so the guarantee is as good as none.

It looks good on paper, but if shit hits the fan, the guarantee of a bond (or the pref share) is as good as the solvency of the issuer.

'Stag' in the ipo context is to subscribe to the ipo for the purpose of selling it on the first day.

Hi all

Super noob here!

how to subscribe to this bond if I do not have a banking account with posb / DBS.

My cdp acct is with OCBC

Thanks!

It's almost the same as dbs. Read above.

LP,

i understand what you mean.

if they cannot pay, and default on the first divd payout. and again, subsequent payout.

is there a penalty for hyflux?

i mean, arent the retail investor protected, by such an event?

Hi foolish chameleon,

I don't think there's any protection for investors of hyflux ordinary shares. As a shareholder, you are taking the up and the downs of the company. Dividends are not guarantee, though some company might have a guidance on the min amt given. I don't think hyflux has it.

As for retail investor of the pref shares/bond, there's already a sort of guarantee. But I wouldn't treat it as one, for the reasons mentioned earlier in our correspondence. Better open both eyes before buying haha

Warm greetings. I was wondering if SingSaver.com.sg can contribute weekly editorials about personal finance? Thank you so very much, Kat.

KATRINA KARIM

VICE PRESIDENT, COMMUNICATIONS

SingSaver.com.sg Ι Singapore’s #1 financial comparison platform

A part of the CompareAsiaGroup Ι Asia’s #1 financial comparison platform

Mobile +65 9844 6618 Ι Email katrina.karim@singsaver.com.sg Ι Skype katrinakarim1 Ι LinkedIn http://bit.ly/1nJ2Nxg

Hi LP, so if issuer is buying back from you at $1 regardless of market price based on par, then what is the point of having "Stag"?

Can you pls use a nickname? I don't know who I'm talking to, thanks.

The point of stag-ing an IPO is that you can do a quick trade and sell within a week to realise those gains. Some IPO are wildly successful, getting 50% gains within a week or more. How is that not a good return as compared to waiting for them to redeem back at par value, which might be a very very long time esp for a perp?

"First redeemable date is on 27th May 2020".

Whatif a scenario they won't redeem and won't pay even if they have the money. All this SOR+ will not make sense. What's the implication to the company other than they can't issue dividend to shareholder ?

Can they continue operation, pay bond or borrow or ... etc ?

Hi BB,

I am a rookie investor and have a noob question about the Hyflux bond. I have purchased the bond but I have no idea how to sell/redeem the bond. I can see it in my CDP/SGX Portofilo but there does not seem to be an option to sell/redeem?

Hi Steve,

First of all, it's not up to you to redeem the bond (technically, it's not a bond either). Either Hyflux redeem it or they don't, and it's not your choice. If you want to sell now, you have to sell it like any other stocks. Go find the ticker symbol, go to your brokerage and sell it. You'll have to pay commission to your broker also.

Post a Comment