Of course, before you can even prepare such statements, you need to keep records. Since you're not listed nor fall under ACRA, you don't have to follow any accounting guidelines nor will you be fined for not meeting standards and regulations, as is the case for public and private companies. Feel free to include or exclude things that don't help you. The first step before you can improve your own situation is to take stock of where you are now. A good record of your financial situation, which involves keeping track of your income and expenses, will allow you to analyse how healthy you are financially.

I've prepared a sample of what a personal income statement looks like in a 3 months period from November to January. I think doing this on a monthly basis is good. However, there are some months that you spend more or less, depending on the holiday season and the variability of your income stream and expenses calender, so you can also consolidate the monthly in quarterly or semi-annually too, to even out the odd months. The statements are really prepared for yourself, so feel free to do anything that makes sense to you.

|

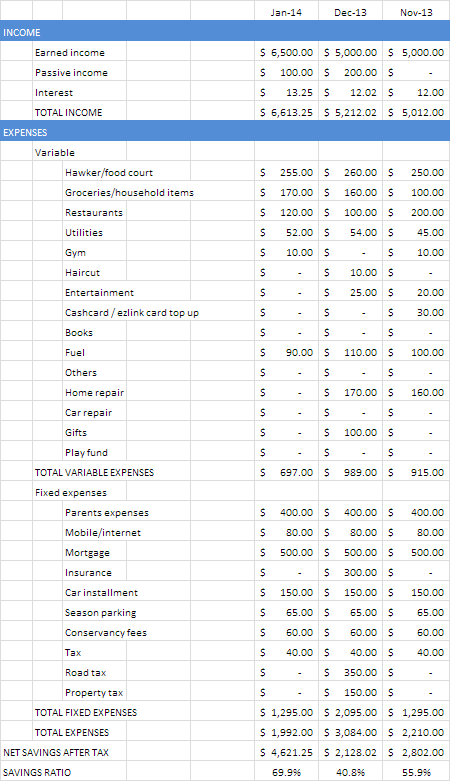

| This is just an example of a personal income statement. The categories for expenses might be useful for your reference though. |

In the income statement for a company, you look at the top line, i.e the revenue. This is equivalent to your total income streams coming either from work that you do or money working for you. Then we have to look at the expenses. Some of them are fixed, some are variable. If you take the revenue minus off the expenses, you'll get the gross profit before tax. That's also your savings if you minus your expenses off your income. After paying taxes, what's left will be your net profit for a company. That's your net savings per year. And this is ultimately what counts at the end of the day, not your gross revenue.

You can further crunch the numbers in the personal income statement to see the following:

1. Percentage change in income (equivalent to % change in revenue)

2. Percentage change in expenses

3. Your savings ratio, which is net savings as a percentage of income (equivalent to profit margin, which is net profit over revenue)

4. Expense ratio, which is total expenses as a percentage of income

Different companies doing different industry will have different profit margin. You can't expect a company in the service industry to have the same profit margin as a manufacturing one. Likewise, different person will have different savings ratio. It depends on how 'light' or how 'heavy' that person's burdens are. Just like there's no meaning to compare the profit margin of a property developer company to that of a shipping company, there's also no meaning to compare the savings ratio between different people. The better way to compare is to compare your own performance metrics across different time periods of your life. For example, you can compare your % income or savings ratio between the year 2008 and the year 2009. The competition should be directed internally, not externally. In other words, you should compare how you do now against how you did in the past, not between how well you do against how well others do.

Remember that savings is like the net profit of a company. You do not want to invest in a company that shows ever increasing revenue but stagnant or decreasing net profits margin, neither do you want to become a person with increasing income but decreasing saving ratio!

A good personal income statement should have the following characteristics:

1. A stable income that is high enough to cover the expenses and then more. This will ensure that there will be some excess left over for savings. Savings is the first step to let your money start working for you. There's no other way that a self-made person can make money work for him without having savings in the first place.

2. Increasing income and decreasing or constant expenses. What's important is not the absolute but the relative. Preferably, the income should increase over time while the expenses are kept constant or increases at a lower rate than the income.

3. Consistent and increasing savings ratio. Savings is all that matters at the end of the day. You work for an income to get the savings; all other expenses can be treated as cost for getting the savings. If you cannot have some savings, you need to increase your income or decrease your expenses. There's no other way around this.

Interestingly, I can imagine a retiree who is not working any more but is drawing down on his assets accumulated over his working years. In such a case, his personal income statement will look extremely unhealthy, with very little revenue on the top line and negative balance each month after subtracting off expenses. But such a person is like a holding company (a company that does not provide a service or produce goods). So, to see if such a company is a good one to invest, you look at the balance sheet and see what kind of assets and liabilities that he owns. I'll talk about balance sheet next in my future posts.

In essence, whatever is described above is really just for a growth company, defined as a company that produces goods or provides a service, and seeking to grow its profits. This is similar to a person who is not retired yet, and not drawing down on his accumulated earnings/assets.

Maybe next time before you get married, you should ask for a person's personal income statements before you choose to invest in him/her LOL

7 comments :

The full amount of mortgage payment should not treated as an expense, even though it is a cash outflow. Only the interest portion of the monthly mortgage installment should be considered an expense. Since this is called a P&L statement, rather than a cash flow statement, it is important to treat the above correctly.

Hi anonymous,

I'm sure you're accounting trained. First of all, thanks for letting me know about this since I'm not accounting trained. However, I would still put the entire mortgage payment instead of the interest only because the personal income statement reports are prepared for myself and I'm ultimately not a company. The personal financial reports should make sense and be useful to me, and putting just the interest part of the mortgage wouldn't fall under this category, haha! In future post, you'll see that I actually treat my income statements somewhat like a cash flow statement. 'Somewhat' because some of the items are accrual and some are not.

LP,

You not only know the Jedi mind trick, you also can use both sides of your brain ;)

Knowing when to unshackle yourself from the black and white precision prison of left-brained thinking, and embracing the fuzzy logic grey sky of right-brained thinking is not easy.

Impressive.

Hi SMOL,

You're always my cheerleader, egging me on :) I did a test on which side of the brain I'm leaning on...turns out that I'm equally dominant on both sides haha!

Here's the test: http://testyourself.psychtests.com/testid/3178

Hi LP,

I like your adaptation on the P&L. If it's our own P&L, we should do it whichever way that serves our tracking purpose. I have a similar record but I placed all the fixed expenses on top and my mum and mum-in-law's allowance are up there as first and second item.

Reason being that it serves to remind me if I don't have to eat, I have to ensure that the two mummies are being taken care of! Haha.

Cheers,

Endrene

Hi EY,

You know what, parent's pocket money is also on the top of the list and also one of the top expenditure I spent monthly :) Oh well, make sure you train your kids to do that as well ;)

Hello Everybody,

My name is Mrs Sharon Sim. I live in Singapore and i am a happy woman today? and i told my self that any lender that rescue my family from our poor situation, i will refer any person that is looking for loan to him, he gave me happiness to me and my family, i was in need of a loan of S$250,000.00 to start my life all over as i am a single mother with 3 kids I met this honest and GOD fearing man loan lender that help me with a loan of S$250,000.00 SG. Dollar, he is a GOD fearing man, if you are in need of loan and you will pay back the loan please contact him tell him that is Mrs Sharon, that refer you to him. contact Dr Purva Pius,via email:(urgentloan22@gmail.com) Thank you.

BORROWERS APPLICATION DETAILS

1. Name Of Applicant in Full:……..

2. Telephone Numbers:……….

3. Address and Location:…….

4. Amount in request………..

5. Repayment Period:………..

6. Purpose Of Loan………….

7. country…………………

8. phone…………………..

9. occupation………………

10.age/sex…………………

11.Monthly Income…………..

12.Email……………..

Regards.

Managements

Email Kindly Contact: urgentloan22@gmail.com

Post a Comment