We all know what's so great about OCBC 360 account. If you hit certain milestone conditions, you get stepped up interest ranging from 0.05% to 1.05%, 2.05% and finally a max of 3.05%. There's some disadvantages to this though:

1. For those who can't change their salary code, you will have to forsake the 1% interest for crediting your salary every month

2. For those who can't pay more than $400 on credit card, you will forsake another 1% interest. I'm sure everyone can hit the $400, but it's how much trouble you want to do to change your status quo.

3. This is up to a max of $50k only.

So, what do I propose?

There's a listed retail bond traded over at sgx with the counter name CapMallA3.8%b220112. Details of the bond are as follows:

1. Coupon issuance dates: Twice a year, Jan and July

2. Underlying: Capitalmall asia

3. Maturity date: First optional redemption 12-Jan-2017 and every year thereafter till 12-Jan-2022 (7 year from now),

4. Face yield: 3.8% every year (1.9% every half year) before 12-Jan-17, thereafter 4.50%

5. Number of payout till maturity: 13

6. Price traded now: $1.028 vs par value of $1.000

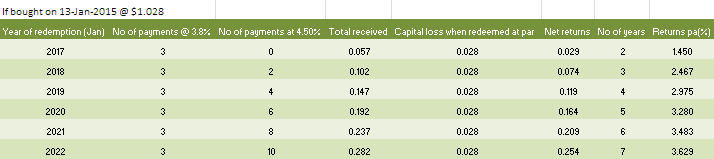

7. Based on the year of redemption, the non-compounded returns are indicated in the table:

(Thanks to SRSI for the gentle reminder of the possibility of early redemption! I forgot about it!)

7. Based on the year of redemption, the non-compounded returns are indicated in the table:

(Thanks to SRSI for the gentle reminder of the possibility of early redemption! I forgot about it!)

So to beat the OCBC 360 rate, we have to bet that the bond is not redeemed at least till 2020, which is 5 years from now. If that happens, we get a annualised non-compounded return of 3.28% if we bought it at today's price of $1.028. If the bond is not redeemed earlier, they will have to mature on Jan 2022, which is 7 year from now. That will get you an annualised return of 3.63% pa.

A few risks needs to be highlighted now:

1. What's the chance of them redeeming the bond?

Capitalmalls asia had the bond set up in Jan 2012. For lack of a better gauge for borrowing costs for companies from banks, I used 3 mths SIBOR to see the risk premium of them borrowing money from investors at 3.8% (which is the face value of the bond). The 3 mths SIBOR back then was 0.39%. So to entice investors to invest, they are giving a premium of 3.41% (3.8-0.39) pa.

There is a step up component of this particular bond. If they did not redeem on 12-Jan-2017 and every year thereafter (until 2022), they will have to pay a higher interest of 4.50% instead of 3.80%, which is an increase of 0.7%. Assuming everything else stays the same, if Capitalmalls asia still has a risk premium of 3.41%, the 3mths SIBOR have to be 1.09% (4.5-3.41) by 2017.

If 3-mth SIBOR is higher than 1.09% by 2017, then the borrowing cost for Capitaland from banks will also rise, making them less likely to redeem back the bond since they have a low cost of borrowing through the bonds. The last time 3 mth SIBOR is 1% or more is back in 2009 before the financial crisis. The current rate now is 0.46% and is very likely to hit 1% in 1 or 2 years time, with the US Fed Reserve set to raise the rates by Q2 or Q3 2015.

I take it that therefore it's unlikely for them to redeem back the bond in 2017. But it's a very simplistic way to see this, I realised. Capitalmalls asia might, for example, not require the debts at all and choose to redeem it.

2. The quality and safety of the bond is as good as the underlying

Capitalsmall Asia is under the big umbrella of Capitaland. To me, a bond by Capitaland family is as good as gold, and as safe as fixed deposit, maybe just a little riskier. The returns stated are non-compounded. To raise it further, you can invest the money received for a higher returns. And technically, I should use XIRR since the cashflow are pretty consistent and even, but I didn't. You can try it out if you wish.

A few risks needs to be highlighted now:

1. What's the chance of them redeeming the bond?

Capitalmalls asia had the bond set up in Jan 2012. For lack of a better gauge for borrowing costs for companies from banks, I used 3 mths SIBOR to see the risk premium of them borrowing money from investors at 3.8% (which is the face value of the bond). The 3 mths SIBOR back then was 0.39%. So to entice investors to invest, they are giving a premium of 3.41% (3.8-0.39) pa.

There is a step up component of this particular bond. If they did not redeem on 12-Jan-2017 and every year thereafter (until 2022), they will have to pay a higher interest of 4.50% instead of 3.80%, which is an increase of 0.7%. Assuming everything else stays the same, if Capitalmalls asia still has a risk premium of 3.41%, the 3mths SIBOR have to be 1.09% (4.5-3.41) by 2017.

If 3-mth SIBOR is higher than 1.09% by 2017, then the borrowing cost for Capitaland from banks will also rise, making them less likely to redeem back the bond since they have a low cost of borrowing through the bonds. The last time 3 mth SIBOR is 1% or more is back in 2009 before the financial crisis. The current rate now is 0.46% and is very likely to hit 1% in 1 or 2 years time, with the US Fed Reserve set to raise the rates by Q2 or Q3 2015.

I take it that therefore it's unlikely for them to redeem back the bond in 2017. But it's a very simplistic way to see this, I realised. Capitalmalls asia might, for example, not require the debts at all and choose to redeem it.

2. The quality and safety of the bond is as good as the underlying

Capitalsmall Asia is under the big umbrella of Capitaland. To me, a bond by Capitaland family is as good as gold, and as safe as fixed deposit, maybe just a little riskier. The returns stated are non-compounded. To raise it further, you can invest the money received for a higher returns. And technically, I should use XIRR since the cashflow are pretty consistent and even, but I didn't. You can try it out if you wish.

Oh, the caveat...you must hold on to the bond until the underlying redeems it at par value. If you do that, you can forget about looking at the market price of the traded bond. If you wish to sell it earlier before it is redeemed, then you have to take what the market gives you. From what I observed so far over 1 yr, the price is pretty stable, whatever the market is doing. Even if the market price drops below your buy price, it's not a concern IF you are holding the bond till maturity.

There you go.

37 comments :

Hi LP

Good post.

Interest rate risk is gone if we can hold it to maturity and seriously it is not too far away and the return is pretty decent.

I didnt know that it was for any amount. I thought it was only for retail investor above 250k. I pm you right now on fb for faster reply. Hehehe

Hi LP a.k.a the Bond guy,

I believe I can answer B's query. The minimum investment is $1,000.

Here's my question:

The bond is callable at par on first date 12 Jan 2017. If the issuer calls for the bond, wouldn't the buyer lose out on the potential coupons and hence the return is lower? :(

Hi B,

I'll answer again here in case readers are also asking the same q. The min amt is 1k for this particular bond because the board lot size is 1000. There are others with board lot size of 100, usually for those with par value of $100.

Retail bonds are traded over sgx like normal shares :) I'm not so rich now to get to trade a quarter million of bonds!!

Hi SRSI,

You caught me! Goodness...I forgot about the early redemption! Let me get back to you on this and also edit the post. From a back of envelope calculation, I think if it redeems at 2017, you'll still get 2.4% pa (damn, lower than ocbc!).

Let me get back to you when I edit my post! Thanks for checking my article!

Hi SRSI,

I hope I did justice to your questions...totally edited the post now. Seems harder to beat the OCBC now lol!

And to correct myself, if redemption is made on 2017, the returns will become 1.45% (boo). I list down the returns based on different redemption yr below:

1. 2017 - 1.45%

2. 2018 - 2.47%

3. 2019 - 2.98%

4. 2020 - 3.28%

5. 2021 - 3.48%

6. 2022 - 3.63%

I included all the coupons received from now (13-jan2015) to the 12th Jan of each redemption year, minus the guaranteed capital loss of investing at $1.028 above par.

Hi LP,

I'll equate the possibility of early redemption to the possibility of OCBC scrapping their 3.6% interest rate. In fact I think the possibility of OCBC scrapping their product is higher because as interest rate rises they will face more competitors while CapMall will have less motivation to do the same.

In addition in order to enjoy OCBC 360 interest rate, the consumer has to perform a series of tasks. If SCB e$aver couldn't even hold at 1.88%, I wonder how OCBC is going to.

Hi Derek,

Good point!

I never really factor in the possibility of OCBC scrapping away their 360 account. Can they do that actually? Maybe they will stop accepting new accounts, but can they actually change the main feature of the account for those who are in it? You will be sure there will be pple howling in protest!

Going along the same line of idea, here's an alternative using non-convertible preference shares:

http://lizardorealm.blogspot.sg/2011/12/non-convertible-preference-shares.html

Similar problem as those retail bonds though as there is a recall/maturity date.

Hi Lizardo,

You ought to update your post, some of the pref shares had already been redeemed back haha!

Totally agree that pref shares, esp from banks, are a good alternative to bonds. It's bond-like in nature, which is what I like about it.

I've written extensively here too: http://bullythebear.blogspot.sg/2013/12/preference-shares-listed-on-sgx.html#.VLUe_yuUfmc

For the investment portfolio for my parents, dubbed LP bonds, I personally put in most of the funds in pref shares by local banks too. When safety of capital is a concern, I don't like the likes of Hyflux/Olam.

I really really wish there's a lot more choices for retail investors without the 250k min.

Hi LP,

I'm pretty sure if you scrutinise the T&C there will definitely be a line that states that the interest rate can change anytime at the bank's discretion. I have SCB e$aver which started off at 1.88% and look at the interest rate now.

Hi Derek,

Ah...it's a passable 1.25% to 1.3% now :( I guess you're right. Good things don't last long. Good credit cards also don't last long...oh well

If I have sudden need for funds, I can close the OCBC 360 account or withdraw the funds (fully / partially) without any penalty at any time. I'm assured of getting back the money without any capital loss unlike the bond which has to be sold in the market at prevailing market price. This is even better than a traditional FD which has penalties for early termination. This is a huge plus for the OCBC 360 account.

LP,

1.3% is promotional rate and I think on incremental balance. The offer then was a fix 1.88% on any balance.

Hi,

Sorry for my ignorance. How does capitalmalls pay you te returns yearly and when they redeem it? Do I buy it the way I buy shares on SCB trading?

Hi anonymous,

Do leave your nickname next time? :)

If you've no idea when you want to liquidate the money, and capital protection is so important, this is probably a wrong instrument. That I will agree.

Did you manage to get the 3.05%?

Hi Derek,

Oh...I see. Indeed suckier than before. Talking about scb, I used to like their Manhanttan card...but now, quite useful. Used to be so good, but their benefits reduced a lot over the years.

Now, it's back to my trusty old posb everyday card lol

Hi anonymous,

Pls leave your nickname behind next time?

Have you bought a shares that pays dividend before? Twice per year one? This will do the same. They will deposit the payments 1.9% every half year, totalling 3.8% per year. All this is till 2017, but I spare you the details.

They do, however, redeem back at $1, no matter what price you bought. Since the price now is at $1.028, you will lose $0.028 when they redeem back the shares. You have to take that into account when you buy bonds that are trading above par value (in this case of $1).

I'm quite sure you can find it from SCB platform since it's traded over the counter.

Hi LP,

Thanks for the reply and your patience. Will leave my nickname next time!(:

Hi anonymous,

See? Haha, I don't know which anonymous I'm talking to...I'm anonymous. No, I'm anonymous. No, I'm anonymous!

LOL!

Most welcomed!

Nice.... why capital mall? Hmmm lots of other good investments better than 360 too... hehe...

Juz a passerby... ;)

Hi LP,

Talking about cash back Credit Cards, I started with Citibank Dividend card but the cash back % was low and you have to accumulate $50 first. Then I switch to Manhattan and like you said, their benefits have reduced over the years. The 'in' card now is OCBC 365 (not to be confused by OCBC 360). Maybe for everyday expenses use OCBC 360 and for very large purchases, the Manhattan.

Hi LP,

Alternatively, One can buy CapMallTrb3.08%210220 retail bond by CapitaMall Trust.

At selling price of 1.017, the yield would be 3.028%

With SGX lowering the retail bond requirement, more company may want to tap into selling to retail investor, considering the interest rate going up soon.

Perhaps can wait for new retail bond to be listed.

Hi Derek,

I'll go check out the card.. Never heard before. Thanks for the intro!

Hi Derren,

That's not how you calculate the yield. If that's the case, then the 3.8% Capitalmall bond, if you buy it at 1.028,shouldnt the yield be 3.8/1.028 = 3.7% pa? You didn't take into acct the capital loss of redemption of bond at par value if you buy it above par.

Capmall 3.08% pays every Aug and Feb. The maturity date is Feb 2014. If you buy it today, you get a total of 13 payments of 1.54% each (3.08/2). I included the payment on maturity date too, though I'm not sure if it's in. The capital loss from redemption from buying the bond above par value is 0.017.

So, the net returns is 13 x 1.54/100 - 0.017 = 0.1832 over roughly 6.5 yrs. So the returns are 0.1832/1.017 divided by 6.5 = 2.77% pa.

The only good thing for this is that there's no early redemption, so there's a lot more certainty.

My take is to invest now and switch later to new bonds, if there are any. They've been talking for a long long time with no action.

Where can you buy the bonds? Is it through brokers like POEMS?

Hi anonymous.

Care to put your nickname next time? Thanks!

You can buy the bonds from brokers like poems, yup. Just look for the counter name.

Hi Bully The BEAR,

I'm new to your blog and the bond market.

Any idea how to buy bonds (both corporate and govt) in SG?

Hi Ray,

There are two kinds of corporate bonds. First is the institutional bonds but that is only for accredited investors. Each bond requires a min of 250k. You need to ask your RM in the bank or broker to help you on that if you're eligible.

The second is retail bonds. These are actually institutional bonds with a smaller tranche for retail investors, and they are also traded over the counter like any stocks in sgx. You can buy them using your brokerage platform like stocks too and there's no min of 250k.

As for govt bonds, you can open an acct with banks (just call them) and then bid for the bonds as and when they are available. It'll be on MAS website and also published on newspaper MONEY section some days before the auction starts. After some time, these bonds will also be traded on sgx also, but these are called the secondary market already, so you're not buying the bond at par value. Usually they will trade above the par value when you buy/sell in the secondary market.

Hope it's clear?

Thanks for the detailed reply :)

I read and re-read your blog post.

There are risks that the bond could be called at par.

The current trading price of this bond is about $1.33

If we buy the bond at today at this price and it gets called back at par, do we still lose money? Sorry I want to calculate but don't know how. :(

Hi Ray,

The price is $1.033, not $1.33.

Now is April, and the bond only pays out the dividend on Jan and July, so this year you would have missed the Jan issuance if you buy it right now. Since the coupon yield is 3.8%pa, this means that every half a year, they will issue 1.9%. The par value is $1.00, so the dividend received every half a year is $0.019. I don’t know when they will redeem it back, but the earliest they can redeem back is 12-Jan-2017. So let’s assume they do redeem it back on 12-jan-2017.

In 2015, if you buy now, you’ll receive 1 coupon payment.

In 2016, you’ll receive 2 coupon payments.

In 2017, you’ll receive 0 payment

So, in total, you’ll get 3 payment @ 1.9% each, so the total received is $0.057 (3*0.019). But if they redeem it, they will redeem it at par. Since you bought it at $1.033, you’ll lose $0.033 (1-0.033).

Net returns = 0.057-0.033 = $0.024

From 1st April 2015 to 12-Jan-2017 is 652 days or 1.786 yrs

So average net returns = 0.024/1.786 = 1.34% pa

That represents the lowest returns you can get because if they choose to redeem it in 2018, they will first boost the payments to 4.5% pa, and you’ll get 2.48% pa.

If in 2019, then will be 3.01% pa and so on and on.

In short, you don’t lose money if you hold it till the bonds are returned. How much you get in return is a big question mark, but minimally you’ll get 1.34% excluding comms.

WOW.

Thanks!

So detailed.

Are you a teacher? LOL

Hi Ray,

Nah, not a teacher. A tutor ;)

no wonder.....

Thanks again for your tutoring :P

Hi LP,

Another question.

Where can I find out all the bonds I can buy?

How do we tell if the bonds are callable or not?

Thanks.

Hi Ray,

You can go to sgx site, under fixed income. I provide the link here:

http://www.sgx.com/wps/portal/sgxweb/home/marketinfo/fixed_income/bonds

You can change the tab from retail bonds, to pref shares and SGS bonds.

To see if they are callable or not, you have to read the prospectus. But you don't have to do the work, I've already done it here: http://bullythebear.blogspot.sg/2013/12/retail-bonds-listed-in-sgx.html#.VRu0vPmUfmc

Do your own due diligence though, I might make a mistake when tabulating.

Hi LP,

Is there an error in your calculation whereby you said in 2017, the payout is 0? I mean even if CMA redeems it on 12 Jan 2017, the arrear of 1.9% for the past 6mths still needs to be paid on 12 Jan 2017 right? Thanks, J.S.

Hi J.S,

I didn't mean no payout in 2017, I meant no payout of 4.5% in 2017 should they redeem by 2017 Jan. There will still be payouts at 3.8% coupon rate for 12-Jan, so you're right. I can't rmb the exact wording, so must read the prospectus for it.

Post a Comment