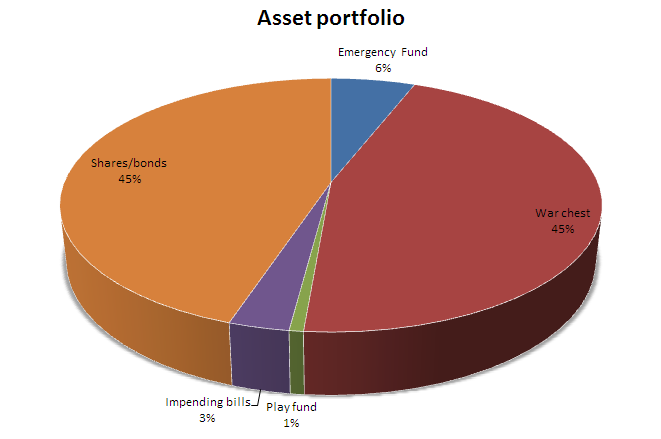

Shares/bonds

This includes the marked to market value of the shares held since the beginning of Jan 2015. Includes all the SGX shares, US and HK portfolio

War chest

I'm almost 50% cash. Some of this are locked in fixed deposit, and none of my warchest comes from CPF. But my war chest is fluid. Every month, it'll increase by a few k and decrease by a few k when I enter a new position. All my monthly savings are actually going into my warchest. Looking at both Derek and my own's ratio of warchest to invested amount, it's kind of hard for the market to crash LOL

Emergency fund

I only have about 3 months emergency fund. This amount of money is mainly held in my SCB account, which is also jointly held by my wife, though only my part of the money is represented here. This account is used to pay for any joint expenses, like housing mortgage, household repair etc. This account serves as my bill paying account for all joint expenses. I'll always keep a fixed amount inside and we do periodically top up to ensure there's enough to pay 3 months worth of household expenses. I know my segregation of emergency funds and bill paying account is not clear, but this is because I had funds for all sorts of things and not a lot of things will catch me by surprise. Kids, don't follow me!

Impending bills

Just for the purpose of this representation, I pulled out my budget for all my big insurance bills that I have to pay for this year and put it under this category. I pay annually, so this is thes single most biggest expense that I have to cater for. The rest are easily settled by either the cashflow from my pay or from the emergency fund/bill paying SCB account that I jointly shared with my wife.

Play fund

Play fund is not a physical account but an accounting account. I put aside a fixed budget every month, for frivolous things like gadgets, games, books etc. As long as it's not a necessity and not for work but for leisure, it'll fall into this account. If I have to travel overseas for holidays, it'll fall under this account too.

I don't have a daily expense account. There's a budget for food and restaurant, so these are properly accounted for and there's no need for a physical account to set aside money for it. Most if not all of it is funded by my pay that comes in weekly or bimonthly. In months where it's drier, I might have to tap into my emergency fund, but I seldom do that. So far, I've only done it once or twice in the driest year of my entire career. Actually my wife can also act as my emergency fund. When she's hitting a dry spot, I'll spend more money on food for her. Vice versa, when I'm having drier months, she'll treat me more often.

My blogging fund comes from my play account. But for some things that need to be paid for, I did a cash call from the cbox community in 2013. They kindly raised enough to make it last till 2019! You can read about my own kickstarter campaign here.

There you go!

17 comments :

Hi AK

Does the expenses for books fall under the play fund?

It's interesting to see how you are almost half in cash/fixed deposit. Certainly a good way to reduce the risk of equity exposure at this point.

Hi B,

Yup, it'll fall under the play fund. Used to be a lot lesser than 50%. It's just that every month my net savings goes into my warchest and it just builds up while waiting for opportunities to arrive ;) Didn't sell any equities since last year.

Hi LP,

When did you change name to AK?

Hi Rolf,

Wah, I've to do a double take to realise what you mean! I thought I've somehow included in my comments the name of that russian gun, before realising you mean figuratively I'm like AK haha!

Nah, I'm not as power as him..I've my own goals which is to have a 240k portfolio generating 5% pa, giving me 1k per month :D I'm still some distance away and you'll see my warchest growing bigger and bigger!

Hi LP,

Thanks for sharing. Seems like we are both waiting to bully the bear. LOL.

A few subtle difference between your portfolio and mine.

I do not have any fix deposits at this moment but I have just sign up for POSB 1.88% and will be moving a part of my Future Funds into it. The rest will remain in a normal deposits account.

My Emergency Fund is 6 months of my basic monthly expenses. I think 3 months for you is fine since you have another half contributing to it.

My daily expense account is the account where my salary is credited into. After allocating my salary into the various account, what is left is for my daily expenses and hence the name.

I almost forgotten about your kick-starter campaign. Maybe I should have one too to pay for my web hosting.

Hi Derek,

Just to clarify, the expenses is for mine alone, not for the entire household :)

Ah, I see, that's where you daily expenses come about :) Either pay yourself first or spend what's remaining..I've tried both before and it works equally well :)

Hey hey, maybe you should try the crowd sourcing method too, haha!

Hi LP,

You are a lucky man to have your wife contributing to your emergency account. kekeke

Crowd sourcing is an excellent idea to generate interest and readership. I'm currently doing a poll on SCB trading account. The numbers are encouraging but if I can get a few thousand more, maybe survey companies will start to take notice and I can ask them to offer freebies to those who take the survey in my site.

Hi LP,

Thanks for sharing your asset allocation. 45% warchest looks big. Are you expecting to employ it anytime soon?

Hi srsi,

Maybe u can do one too? Haha

The warchest is a opportunity fund. It'll be deployed when there is opportunity. I've no time line for that deployment so not really expecting anything ha ha!

Hi LP,

Let's encourage our fellow bloggers to blog about their asset allocation. It will be interesting to see how different or similar it is to ours.

Hi Derek,

Agree :)

Hi LP,

Wow! So much cash in the warchest. Are you expecting any sort of crisis coming soon? STI has just hit new 52 week highs and probably its good to keep more cash for opportunities :)

Hi Secretinvestors,

Nah, not expecting any :) The uncles and aunties haven't start recommending stocks to me yet, and I'm sure a lot of pple have a lot of warchest, so that implicitly means the crash is not going to happen soon :)

There's a difference between selling current stock holdings to fatten one's warchest and building up one's warchest through savings. I'm not doing the former, so it will naturally build up as I put more savings into it ;)

wow that's almost half your portfolio in cash...

what happens if the market continues to move sideways or upwards in the coming 3-5 years?

how will u handle this kinda situation?

Hi Felix,

I never really feel a need to spend that warchest. It's an opportunity fund, so if there's opportunities, I'll seize it. If there's nothing to do, I don't do anything with it. Periodically things would happen, and I'll use it. The most recent utilisation of the warchest is the purchase of Sheng siong, St eng and Sci. I'm still waiting to get more but only at the right price.

So if the market goes up. I'll build up more warchest. If it goes down, I'll buy more :)

Hi K,

Thanks for sharing! It's true isn't it? A lot of people are holding a lot of cash, waiting to be deployed. How to crash? Lol!

Post a Comment