Business

Starburst is a Singapore based engineering group that specializes in design and engineering of firearms-training facilities. They have a track record of 15 yrs in the industry. Their 3 main business segments are

1. Fire arm shooting ranges - They design, fabricate and install their proprietary anti-ricochet ballistic protection systems for indoor, outdoor and modular live firing range, close quarter battle houses and method of entry training facilities. It's not stated anywhere that they are involved in the firing range that I went to in my last reservist, but from the pictures provided in the IPO prospectus, I'm quite sure they are involved.

2. Tactical training mock ups - They design, fabricate and install those simulations scenario, like sniper tower and counter terrorism operation training

3. Maintenance services and others - Basically design, supply and fabricate structural and architectural steel works, also maintain facilities.

Among the 3 segments, this is the one that is recurring in income. The other two are one-off and therefore their revenues are going to be lumpy. They stated that they are going to increase their maintenance services segment so as to provide more earnings visibility. I think that's a good move. The other business segments doesn't provide that kind of assurance to investors.

| Revenue breakdown | FY2013 | FY2012 | FY2011 | |

| Firearm shooting ranges | 14639 (69.6%) | 16188 (93.4%) | 21211 (93.3%) | |

| Tactical training mock ups | 3460 (16.4%) | - | 351(1.5%) | |

| Maintenance services and others | 2946 (14%) | 1149(6.6%) | 1172(5.2%) | |

Ratios

Take a look at their ratios:

| FY2013 | FY2012 | FY2011 | ||

| ROE | 33.7 | 47.7 | 72.6 | |

| Profit/revenue (net margin) | 41.5 | 37.3 | 26.4 | |

| Revenue/Asset (asset turnover) | 0.523 | 0.930 | 1.120 | |

| Assets/equity (leverage) | 1.554 | 1.376 | 2.451 | |

| EPS based on post IPO share base | 3.49 | 2.59 | 2.41 | |

The kind of business they are doing certainly have huge margins! You're talking about 26 to 41% net margins here! ROE is a strong double digit for the last 3 years. I think in FY2011, the ROE is artificially raised because of the higher leverage which they used (look at their assets/equity of 2.451 in FY2011 vs 1.554 in FY2013).

EPS of 3.49 cts in FY2013, and their IPO price of $0.31, means that their PER is about 8.8 times, which is not excessive. What's the weighted average PE of STI index? It's 15.1, according to this. Starhub has a PE of 19.4 while DBS has a PE of 11.3, to give you a feel of the PE ratio of different big companies you know. The NAV before adjusting for the IPO proceeds is 12.94 cts, so the P/B is about 2.4. ST Engineering, a company with about the same industry as Starburst, has a PE of 20.4 and a PB of 5.29.

Revenue

| FY2013 | FY2012 | FY2011 | ||

| Revenue | $21,045 | $17,337 | $22,734 | |

| Profit before income tax | $10,107 | $7,641 | $7,145 | |

| Cost | $10,938 | $9,696 | $15,589 | |

| Finance cost | $82 | $135 | $308 | |

| Project/production cost | $8,412 | $6,682 | $11,558 | |

| Net profit | $8,729 | $6,464 | $6,013 | |

Revenue is lumpy, given the variability of the contracts they can secure in their order books The cost seems very contained, giving them a very high profit margins. The majority of the cost is the project/production cost, accounting for about 70 to 80% of the cost. Take note that a majority of their employees are foreign workers (77% as of 31st Dec 2013), so they are also going to face the same issue as all SME with regards to the labour policy and shortage.

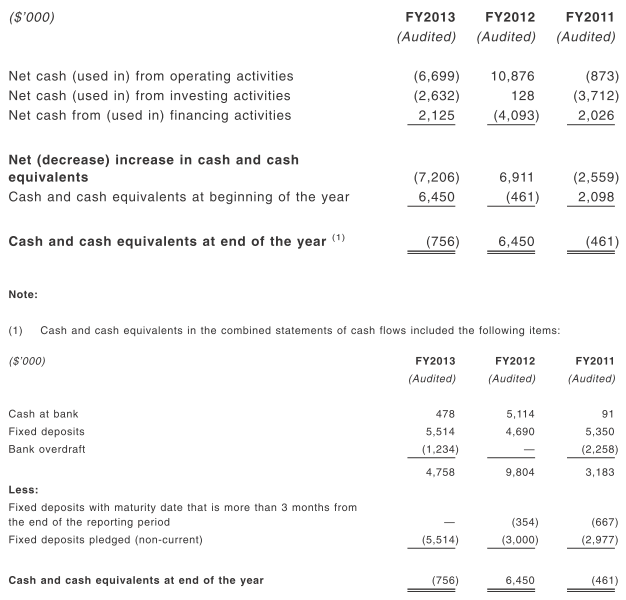

Cash flow

Operating cash flow is again lumpy, and highly dependent on whether they secure projects. The payment for the projects are based on percentage of completion, and the contracting party can retain 10 to 20% of contract sum upon completion of works in order for them to assess shoddy work or work-yet-to-be completed. I guess that's standard practice, like all construction firms. I'm not very good at analysing cash flows, so I won't even try.

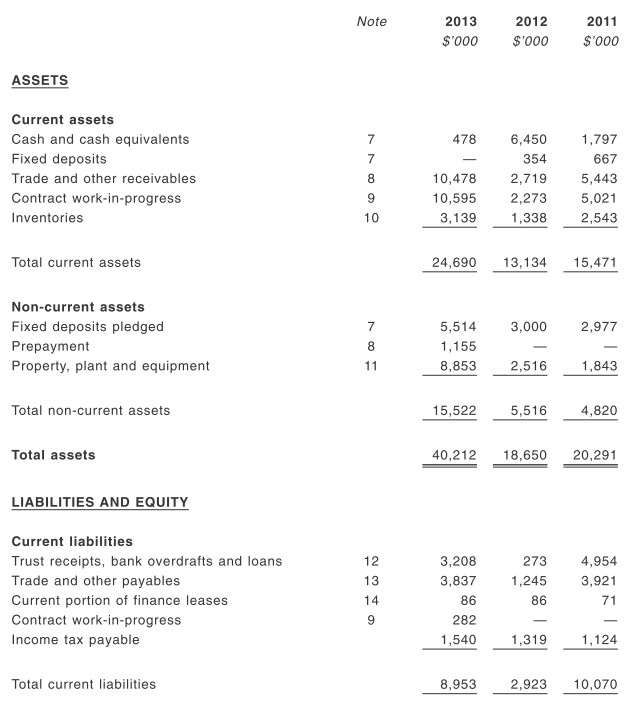

| FY2013 | FY2012 | FY2011 | ||

| Assets | $40,212 | $18,650 | $20,291 | |

| Current | $24,690 | $13,134 | $15,471 | |

| Non-current | $15,522 | $5,516 | $4,820 | |

| Liabilities | $14,331 | $5,096 | $12,011 | |

| Current | $8,953 | $2,923 | $10,070 | |

| Non-current | $5,378 | $2,173 | $1,941 | |

| Total equity | $25,881 | $13,554 | $8,280 |

But based on their balance sheet, their current ratio is pretty healthy. But not all their current assets can be liquidised to pay off short term debts. Let's see the breakdown of their assets:

I think most of their operating cashflow in FY2013 is locked up in the form of contract work in progress and also other receivables. Once they convert that to cash, their operating cash flow should improve greatly. But in the meantime, I don't think they have issues with paying off any short term debts. Their receivables turnover for FY2011, FY2012 and FY2013 is 55, 16 and 10 days respectively. They said it's attributable to their stringent internal controls policy...okay, anyway, it seems really alright.

Dividends?

Any dividends? They are giving out at least 20% of their profit after tax as dividends in FY2014. Their order book for the firearm shooting ranges and tactical training mock ups is 19.7 million, which will be translated into revenue over the next one year (it's about there, if you add up the trade and other receivables and the contract work-in-progress for FY2013, you'll get about 20 million). As for maintenance services, they said that it'll be approximately 26.1 million, which will be translated over the next 1 to 19 years. I don't think you can add up 19.7 million to 26.1 million to give you 45.8 million in order book for FY2014. I'll just divide 26.1 million by 19, THEN add to the more or less confirmed 19.7 million, to give a estimated revenue of FY2014 as 21 million. That's also about the same revenue as that earned in FY2013.

Their net margin is about 40%, so that means their profit after tax in FY2014 is about 0.4 x 21 = 8.4 million. 20% of that will be distributed as dividends, so that's about 1.68 million, or 0.672 cts per share. The offer price is 31 cts, so that's going to give us a dividend yield of around 2.17% pa. Ah, you have to compare with ST engineering, which gives a yield of about 1.8% pa. This is after all a 'growth' company, so don't expect lofty yields of 5 to 6%. You should be looking at capital gains instead.

Competitive advantage

They listed down their local competitors, namely Cubic Range (listed in US), Meggitt Training systems (pte), Microcircuit systems (pte). The industry is such that a main contractor will bid successful for a project, then they will sub tender to others, so there's a fair amount of cooperation between all the competitors. As for Cubic range, I read through their annual reports but it's not a fair comparison since they do a ton of other things as well. If you must know, their latest net margin is about 1.4% only, compared to Starburst's 30 to 40% net margin.

There are of course other competitors internationally, since Starburst is also going overseas in middle east to bid for contracts.

Their main advantage over the others seems to be that they can fabricate and install bullet containment systems using their proprietary IP. I don't know how great that is, but from their net margins, it does appear to be quite unique. If only I knew about the margins of the other players...

The defense industry is likely to be very recession proof. I just don't see defense budget being cut...at best it'll be kept the same. And we're talking about big players - government or defense ministry - who command huge budgets. I think it's a good industry to be in with huge barriers of entry. You can't just apply to build such things because you need to have a good track record and have the relevant certification level, and Starburst's 15 years of experience in the industry should count for something.

Why are they doing it?

The two founders are going to hold 80% of the shares, with the remaining 20% of the shares (all 50 million of them) for the public. In the IPO, only 4% (a mere 2 million) of the public tranche is for retailers in the IPO. The remaining 48 million are up for placements. As usual, the controlling founders cannot sell their shares before the six months period is up. They must also hold at least 50% of their holdings for another six months.

A big part of the proceeds (all 45% of it) is going to be for acquisition of leasehold land and buildings. The next big part (37%) is for general working purposes. I just don't know why they want to IPO it. Perhaps the two founders want to take back their capital and liquidise their holdings (don't they all?)

Worth getting?

I think this is fairly valued, and certainly not a sucker's deal. But the problem is getting enough of it to matter during the IPO. In the IPO, it's likely to be very hot, given the low 4% available for us mere mortals to bid. With 20% of available shares available for trading in the first 6 months, I think this is going to be those illiquid counters with huge movements. I'm going to take a second look once it's properly listed and all. Closing is on 8th July 12 noon. Trading will start next Thurs, 10th July.

13 comments :

Hi LP,

That's a very good and comprehensive analysis of Starburst. As you have mentioned, on the surface, they do appear to have some moat and the valuation is not demanding.

Will be taking a closer look at it after it lists since getting one lot at IPO is pretty meaningless.

Hi 15HWW,

Yea, it's certainly worth a second look. Maybe can punt for a stag lol

Hi LP

I think the reason why they would want to ipo 20% of it is mainly to raise capital for obviously leasehold land and working capital purposes.

If you see at the ending cash and cash equivalent as of 2013 it is actually at a negative and due to the nature of their industry of having to recognize these revenue and collect receivables based of percentage completion, it appears that the company might in need of a cash.

A lot is perhaps down to how they are going to structure their working capital and sustain the healthy level of margins they are getting right now. Fair risk to me but growth potential might be there.

LP,

I was hopping no one blogs about it. Let it slip under the radar and I can increase my chances.

Now that the cover is blown. Its everybody game.

*hmm..seems like I'm hyping it up further. LoL

Cheers!

Derek

PS: I'm having a hard time deciphering the words for verification.

Once again, a really good write-up by LP. Thanks alot for the comprehensive coverage. Been following your posts since the AIMS REIT Rights issue. Always easy to read, digest and understand. Keep it up please.

Hi B,

Thanks for your input. I know my weakness is at cash analysis - I don't have enough accounting knowledge to make sense of the numbers. Argh..But i'll work on it lol

Regarding the negative cash flow in FY2013, I think most of their cash are tied up in the half completed work under their balance sheets. I also think they have little problems collecting money from them from the short record they provided so far.

But to do a IPO just to raise cash for general working purposes...why not borrow? There's interest to be paid but I don't know..I think the real reason is that the founder wants to cash out. I also don't understand why a company like Hock Lian Seng wants to do an IPO too.

Oh well, some things we don't have to understand. Ultimately, we just have to decide if this is a good buy, lol

Hi Derek,

LOL, you are interested too? Nah, I don't have the power to hype up - my blog is not so popular like AK's haha

Good luck for your IPO - I've not decided whether to punt it or not yet :)

Yeah, I know about the verification. It's the same when I comment on other blogs. Sometimes I've to refresh again and again just to see what the words/numbers are.

Hi Eugene,

Ah..thanks so much for your encouragement :)

Haha, my specialty is in rights issue for reits because I've been doing that so many times. FA on company stocks? Nah, very much less so.

Hi LP,

I think the main concern here would be growth. Oh yes, thanks for a very comprehensive summary of the IPO and also the financial metrics of this business.

Being so niche, I wonder what the growth prospects are like? Granted their ROE is off the charts and that NPM is also very high, but based on the nature of their business (i.e. contractual), it would be tough to gain any visibility into future prospects so as to forecast revenues.

Their CFS is also rather rather lumpy, and you don't get much assurance that they can consistently generate FCF.

In short, I will take a wait and see attitude before I conclude that the business has a "moat".

Regards.

Hi mw,

Thanks for your input :)

I agree with you. The only thing that is missing is the track record of them being able to generate contracts regardless of recession. Otherwise, there's no earnings visibility, revenue and cashflow becomes lumpy and we start to see their metric dropping like flies. It's hard to make any forecast in this kind of business.

They did say they are trying to get more even revenues per year by going more into their maintenance business segment. Not sure how that will pan out in the near future.

Applied 51 lots...didn't get any. Oh well...those who got any sure huat because it's only about 10 to 16% chance of getting it. 400+ times oversubscribed! LOL

any update on Starburst? just noted the company buy back it own share last week

Hi,

Sorry, didn't really keep track of the results after they ipo-ed. Didn't seem very good though.

Post a Comment